In dwelling policies, automatic increase in insurance is a valuable feature that policyholders should understand to ensure they maintain adequate coverage. This mechanism is designed to adjust your coverage limits automatically, keeping pace with inflation and rising costs of construction and repairs. It's a practical solution for homeowners who want to safeguard their properties without constantly monitoring and updating their policies. By knowing how this feature works, you can make informed decisions about your insurance needs and avoid potential pitfalls associated with underinsurance.

The automatic increase in insurance feature is particularly beneficial in today's fluctuating economic landscape. With the costs of materials and labor rising, the expense of rebuilding or repairing a home can quickly surpass the initial coverage amounts set in a policy. This automatic adjustment helps policyholders maintain a safety net, ensuring that their insurance will cover the real cost of restoring their home after a loss. It's a proactive approach that aligns the coverage with the current market conditions, providing peace of mind for homeowners.

Understanding the nuances of in dwelling policies automatic increase in insurance is essential for making the most of this feature. Not all insurance policies automatically include this provision, and the specifics can vary between providers. By examining the terms of your policy and discussing options with your insurance agent, you can tailor your coverage to better suit your personal circumstances and financial goals. It's an opportunity to optimize your insurance strategy, ensuring that your home is adequately protected against unforeseen events.

Table of Contents

- Introduction to Dwelling Policies

- What is Automatic Increase in Insurance?

- How It Works: The Mechanics of Automatic Increase

- Benefits of Automatic Increase in Dwelling Policies

- Potential Drawbacks and Limitations

- Evaluating Your Need for Automatic Increase

- Comparing Policies: Automatic vs. Manual Adjustments

- Understanding Coverage Limits and Inflation

- Factors Influencing Insurance Adjustments

- Role of Insurance Providers in Automatic Increase

- Customizing Your Insurance Policy

- Legal and Regulatory Considerations

- Real-Life Examples and Case Studies

- Frequently Asked Questions

- Conclusion: Making the Most of Your Insurance Policy

Introduction to Dwelling Policies

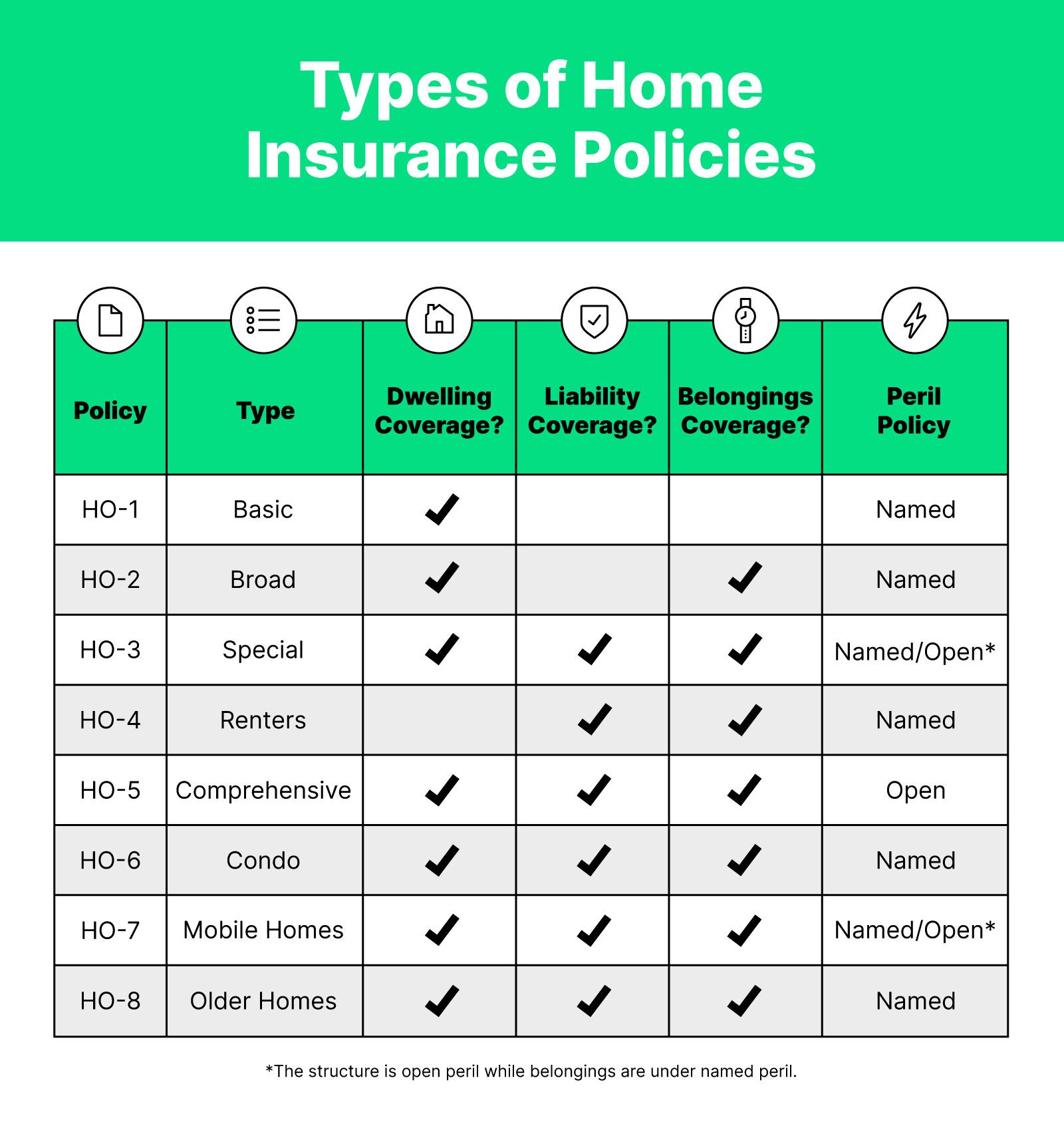

Dwelling policies are a cornerstone of homeowners insurance, providing coverage for the physical structure of a home. These policies are crucial for protecting one of the most significant investments an individual can make. Understanding the different types of dwelling policies is essential for selecting the right coverage. Generally, dwelling policies cover damages caused by specific perils such as fire, wind, or theft. However, the extent of coverage can vary significantly depending on the policy type and provider.

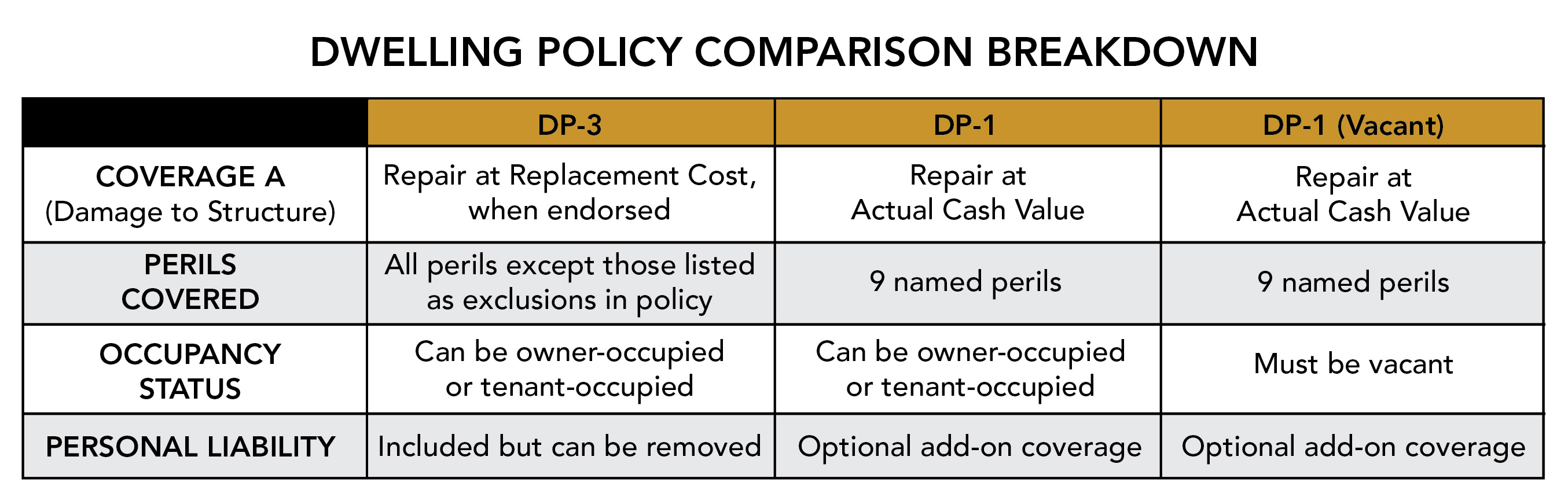

There are primarily three types of dwelling policies: DP-1 (Basic), DP-2 (Broad), and DP-3 (Special). The DP-1 policy offers limited protection and is often the most affordable option. It covers named perils, which means it only insures against events specifically listed in the policy. The DP-2 policy provides broader coverage with a more extensive list of perils. Finally, the DP-3 policy is considered the most comprehensive, offering all-risk coverage for the structure, meaning it covers all perils except those explicitly excluded.

Choosing the right dwelling policy involves assessing your specific needs and financial situation. Factors such as the age and condition of the home, geographic location, and personal risk tolerance should all be considered. Additionally, understanding the policy's coverage limits, deductibles, and exclusions is crucial to ensure you are adequately protected without overpaying for unnecessary coverage.

What is Automatic Increase in Insurance?

The automatic increase in insurance is a policy feature designed to adjust the coverage limits of a dwelling policy automatically. This adjustment accounts for inflation and increases in construction costs, ensuring that the policyholder maintains adequate coverage over time. Without this feature, a homeowner may find themselves underinsured, which can lead to significant financial strain in the event of a loss.

Automatic increase in insurance is typically implemented as a percentage increase in coverage limits each year. This percentage is based on various factors, including inflation rates and trends in construction costs. By allowing the coverage to grow with these external factors, policyholders can avoid the pitfalls of stagnant coverage limits in a dynamic economic environment.

This feature is especially beneficial for long-term policyholders who may not regularly review or adjust their coverage. It provides a level of protection against the erosion of purchasing power and ensures that the policy remains relevant and effective. In essence, automatic increase in insurance acts as a safeguard, keeping coverage in line with the true cost of repairing or rebuilding a home.

How It Works: The Mechanics of Automatic Increase

Understanding how the automatic increase in insurance works is key to appreciating its value. At its core, this feature is a systematic adjustment of the policy's coverage limits, designed to keep pace with economic changes. The mechanics involve several components working together to provide continuous protection.

Typically, the process begins with the insurance provider determining a baseline percentage for the increase. This percentage is often based on economic indicators such as the Consumer Price Index (CPI) or specific indexes related to construction costs. Once established, this percentage is applied annually to the policy's coverage limits, resulting in an automatic increase without requiring any action from the policyholder.

Moreover, the automatic increase mechanism may include periodic reviews by the insurance company to ensure the adjustments remain accurate and beneficial. During these reviews, the provider may reassess the percentage used for increases and make necessary adjustments to align with current economic conditions. This ongoing evaluation helps to maintain the integrity and effectiveness of the policy over time.

Benefits of Automatic Increase in Dwelling Policies

The benefits of incorporating an automatic increase in dwelling policies are manifold. For one, it offers peace of mind to homeowners by ensuring that their coverage remains sufficient to cover the costs of potential losses. As the cost of materials and labor continue to rise, automatic increases help to close the gap between insured amounts and actual reconstruction costs.

Additionally, automatic increases reduce the administrative burden on policyholders. Without this feature, homeowners would need to periodically review and adjust their policies to maintain adequate coverage. This can be a time-consuming and complex task, requiring knowledge of current market conditions and potential future trends. Automatic increases simplify this process, allowing homeowners to focus on other aspects of their lives.

Furthermore, automatic increases can enhance the overall value of an insurance policy. By keeping coverage limits aligned with economic realities, policyholders can avoid the financial pitfalls of underinsurance. This proactive approach not only protects the homeowner's financial interests but also contributes to the long-term stability and resilience of their insurance strategy.

Potential Drawbacks and Limitations

While the automatic increase in insurance offers significant advantages, there are also potential drawbacks and limitations to consider. One potential issue is the increase in premium costs associated with higher coverage limits. As the coverage amount rises, so too does the premium, which can strain a homeowner's budget.

Another limitation is the potential for over-insurance. In some cases, the automatic increases may result in coverage limits that exceed the actual replacement cost of the home. This can lead to unnecessarily high premiums and wasted financial resources. It's important for policyholders to periodically review their coverage and adjust the automatic increase settings if necessary.

Additionally, automatic increases may not account for all factors influencing the cost of rebuilding or repairing a home. For instance, regional variations in construction costs or changes in building codes may not be fully reflected in the automatic adjustments. Homeowners should be aware of these limitations and consider supplementing their coverage with additional endorsements or riders if needed.

Evaluating Your Need for Automatic Increase

Determining whether the automatic increase in insurance is right for you requires a thoughtful evaluation of your personal circumstances and financial goals. Begin by assessing the current coverage limits of your dwelling policy and comparing them to the actual replacement cost of your home. This analysis can help identify any potential gaps or areas of concern.

Consider your long-term plans for the property. If you intend to remain in the home for an extended period, automatic increases can provide valuable protection against inflation and rising costs. However, if you anticipate selling the home or making significant renovations, you may need to tailor your coverage to reflect these changes.

It's also important to weigh the cost of automatic increases against your budget. Evaluate the impact of higher premiums on your finances and determine whether the benefits of increased coverage justify the expense. Consulting with a trusted insurance advisor can provide additional insights and guidance, helping you make an informed decision.

Comparing Policies: Automatic vs. Manual Adjustments

When considering dwelling policies, it's essential to compare the benefits and drawbacks of automatic increases versus manual adjustments. Both approaches have their merits, and the right choice depends on your individual needs and preferences.

Automatic increases offer convenience and peace of mind, ensuring that coverage limits remain aligned with economic trends without requiring intervention from the policyholder. This can be particularly advantageous for homeowners who prefer a hands-off approach to insurance management.

On the other hand, manual adjustments provide greater control over the policy's terms and conditions. Homeowners who choose this approach can tailor their coverage to reflect specific changes in their circumstances, such as renovations or changes in regional construction costs. However, this method requires a proactive approach and regular monitoring to ensure adequate protection.

Ultimately, the decision between automatic increases and manual adjustments depends on your risk tolerance, financial goals, and willingness to actively manage your insurance policy. By carefully considering the pros and cons of each option, you can select a strategy that aligns with your needs and priorities.

Understanding Coverage Limits and Inflation

Coverage limits are a fundamental aspect of any dwelling policy, defining the maximum amount the insurer will pay in the event of a covered loss. These limits are crucial for ensuring that the policyholder has sufficient resources to repair or rebuild their home following a disaster.

Inflation can significantly impact coverage limits, as rising costs of materials and labor can quickly outpace the original amounts specified in the policy. Without adjustments, a homeowner may find themselves underinsured, facing significant out-of-pocket expenses to cover the shortfall.

Automatic increases in insurance address this issue by periodically adjusting coverage limits to reflect current economic conditions. By keeping pace with inflation, these adjustments help to maintain the purchasing power of the policy and ensure that the homeowner remains adequately protected over time.

Factors Influencing Insurance Adjustments

Several factors influence the adjustments made to dwelling policies through automatic increases. Understanding these factors can help homeowners appreciate the rationale behind the changes and ensure that their coverage remains appropriate for their needs.

One primary factor is the rate of inflation, which directly affects the cost of materials and labor required for home repairs. As inflation rises, the cost of rebuilding a home increases, necessitating higher coverage limits to maintain adequate protection.

Additionally, regional variations in construction costs can influence automatic adjustments. Factors such as local economic conditions, supply chain disruptions, and changes in building codes can all impact the cost of repairs and replacements, affecting the necessary coverage limits.

Insurance providers also consider historical data and trends when determining the percentage for automatic increases. By analyzing past patterns and projections, insurers can make informed decisions about the appropriate adjustments to keep coverage aligned with current realities.

Role of Insurance Providers in Automatic Increase

Insurance providers play a pivotal role in implementing and managing automatic increases in dwelling policies. Their expertise and resources are essential for ensuring that the adjustments remain relevant and effective in a dynamic economic environment.

Providers begin by analyzing economic indicators and market trends to determine the appropriate percentage for automatic increases. They consider factors such as inflation rates, construction costs, and regional variations to arrive at a figure that reflects current conditions.

Once the percentage is established, providers apply it to the policy's coverage limits, resulting in an automatic adjustment. They may also conduct periodic reviews to ensure that the increases remain beneficial and aligned with the homeowner's needs.

Insurance providers also play a critical role in educating policyholders about the benefits and limitations of automatic increases. By providing clear and comprehensive information, they empower homeowners to make informed decisions about their coverage and optimize their insurance strategy.

Customizing Your Insurance Policy

Customizing your dwelling policy to include or exclude automatic increases requires a thoughtful approach to ensure that the coverage aligns with your specific needs and financial goals. Begin by reviewing your current policy and understanding the terms and conditions related to automatic increases.

If your policy does not currently include automatic increases, consider discussing this option with your insurance provider. They can provide insights into the benefits and potential costs associated with this feature, helping you determine whether it is a suitable addition to your policy.

For homeowners who already have automatic increases in place, it's essential to periodically review the coverage limits and adjustments to ensure they remain appropriate. Consider factors such as changes in the home's value, regional construction costs, and your long-term plans for the property when evaluating the policy.

By customizing your insurance policy, you can optimize your coverage to better reflect your individual circumstances and protect your financial interests. Working with a trusted insurance advisor can provide additional guidance and support throughout the process.

Legal and Regulatory Considerations

When considering automatic increases in dwelling policies, it's important to be aware of the legal and regulatory considerations that may impact your coverage. Insurance is a highly regulated industry, and policies must comply with state and federal laws to ensure consumer protection and fairness.

Regulations governing automatic increases may vary by jurisdiction, with some states imposing specific requirements or limitations on the adjustments. It's essential for homeowners to understand the legal framework surrounding their policy and ensure that any automatic increases comply with applicable laws.

Additionally, policyholders should be aware of their rights and responsibilities under the terms of their dwelling policy. This includes understanding the process for disputing or appealing adjustments, as well as the procedures for modifying or canceling the automatic increase feature if desired.

By staying informed about the legal and regulatory aspects of automatic increases, homeowners can navigate the complexities of the insurance landscape with confidence and ensure that their coverage remains compliant and effective.

Real-Life Examples and Case Studies

Real-life examples and case studies can provide valuable insights into the practical applications and benefits of automatic increases in dwelling policies. By examining these scenarios, homeowners can better understand how this feature can protect their financial interests and enhance their insurance strategy.

In one case study, a homeowner in a rapidly growing metropolitan area experienced a significant increase in property values and construction costs. Thanks to the automatic increase feature in their dwelling policy, their coverage limits adjusted accordingly, allowing them to rebuild their home without financial strain after a catastrophic fire.

Another example involves a homeowner in a region prone to natural disasters. By incorporating automatic increases into their policy, they were able to maintain adequate coverage despite rising costs associated with frequent repairs and rebuilding efforts. This proactive approach provided peace of mind and financial security in the face of ongoing challenges.

These examples illustrate the tangible benefits of automatic increases in dwelling policies, highlighting their ability to adapt to changing circumstances and protect homeowners' investments over time.

Frequently Asked Questions

How does the automatic increase feature affect my premium?

The automatic increase feature can result in higher premiums, as the coverage limits are adjusted to reflect rising costs. However, the increased protection and peace of mind often justify the additional expense.

Can I opt-out of automatic increases in my dwelling policy?

Yes, many insurance providers allow policyholders to opt-out of automatic increases if desired. It's important to carefully consider the potential risks and benefits before making this decision.

How do insurance providers determine the percentage for automatic increases?

Insurance providers typically base the percentage on economic indicators such as inflation rates and construction cost trends. They may also consider regional variations and historical data to arrive at an appropriate figure.

What happens if the automatic increase results in over-insurance?

If the automatic increase results in over-insurance, policyholders may end up paying higher premiums than necessary. It's important to periodically review coverage limits and make adjustments if needed to ensure appropriate protection.

Are automatic increases applied to all aspects of my dwelling policy?

Automatic increases are typically applied to the coverage limits for the physical structure of the home. However, additional endorsements or riders may be necessary to cover other aspects, such as personal belongings or liability protection.

How can I ensure that my dwelling policy remains compliant with legal requirements?

To ensure compliance, review the terms of your policy and any applicable regulations in your jurisdiction. Consult with your insurance provider or a legal advisor if you have questions or concerns about the legality of your coverage.

Conclusion: Making the Most of Your Insurance Policy

The automatic increase in dwelling policies insurance is a powerful tool for ensuring that homeowners maintain adequate coverage in the face of rising costs and inflation. By understanding how this feature works and evaluating its potential benefits and limitations, policyholders can make informed decisions about their insurance strategy.

Whether you choose to incorporate automatic increases into your dwelling policy or prefer a more hands-on approach with manual adjustments, the key is to remain proactive and engaged in managing your coverage. By regularly reviewing and customizing your policy, you can optimize your protection and safeguard your financial interests over time.

Ultimately, the automatic increase in insurance is an opportunity to enhance the resilience and stability of your dwelling policy, providing peace of mind and security for you and your family. By making the most of this feature, you can confidently navigate the complexities of the insurance landscape and protect your most valuable asset—your home.

For more information on dwelling policies and automatic increase features, you may visit this external resource.

You Might Also Like

Tom McEnery: The Visionary Behind San Jose's TransformationRevealing The Success Story Of Jos� Mas: A Visionary Leader

Empowering Mothers: The Role Of Social Media In Modern Parenting

Engage With The Foro Shiba Inu Community: Connect And Learn

Original Props From Star Wars: Treasures Of The Galactic Saga

Article Recommendations

- Charlie Pride The Iconic Country Singers Age And Legacy

- Did Machine Gun Kelly And Megan Fox Lose A Child A Closer Look

- Cole Ballards Dad Everything You Need To Know