A mortgage note is a pivotal financial document that serves as a written promise to repay a loan secured by a mortgage. It's crucial for both lenders and borrowers, outlining the key terms of the loan agreement, including the principal amount, interest rate, and repayment schedule. Understanding the nuances of a sample mortgage note can offer significant insights into the mortgage process and help ensure that all parties involved are aware of their obligations and rights.

In the realm of real estate transactions, the sample mortgage note acts as a critical piece of the puzzle. It not only formalizes the borrower's commitment to repay the loan but also provides the lender with a legal instrument to enforce that commitment. For those new to the mortgage world or looking to refinance, diving into the intricacies of a sample mortgage note can be both enlightening and empowering. This document, despite its complexity, is essentially a guide to the financial relationship between borrower and lender, ensuring transparency and trust.

Given the importance of mortgage notes, it's imperative to comprehend their structure and content fully. This article will explore the essential components of a sample mortgage note, offering a comprehensive understanding for anyone involved in a mortgage transaction. Whether you're a potential homebuyer, a real estate professional, or simply curious about mortgage documentation, this guide will provide valuable insights into the world of mortgage notes, helping you navigate the real estate market with confidence and clarity.

Table of Contents

- What is a Mortgage Note?

- Components of a Sample Mortgage Note

- Importance of Sample Mortgage Notes

- How to Draft a Sample Mortgage Note

- Legal Considerations in Mortgage Notes

- Sample Mortgage Note vs. Promissory Note

- Interest Rates and Repayment Terms

- Default Clauses and Foreclosure

- Record Keeping and Documentation

- Challenges in Understanding Mortgage Notes

- Frequently Asked Questions

- Conclusion

What is a Mortgage Note?

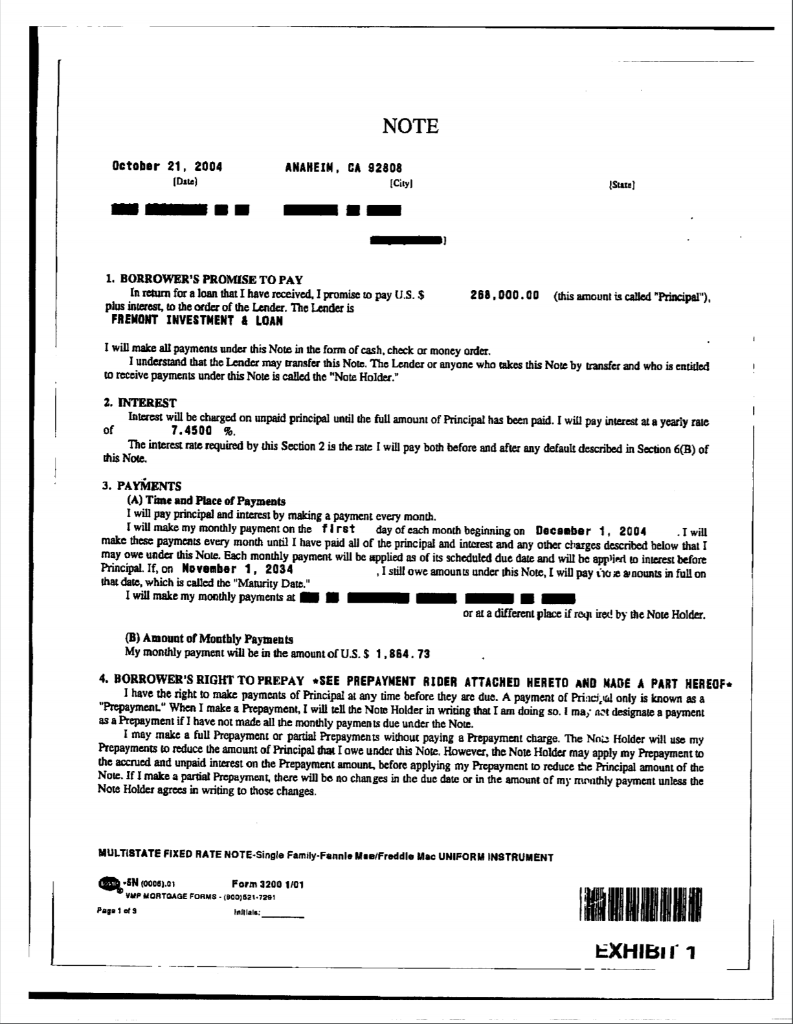

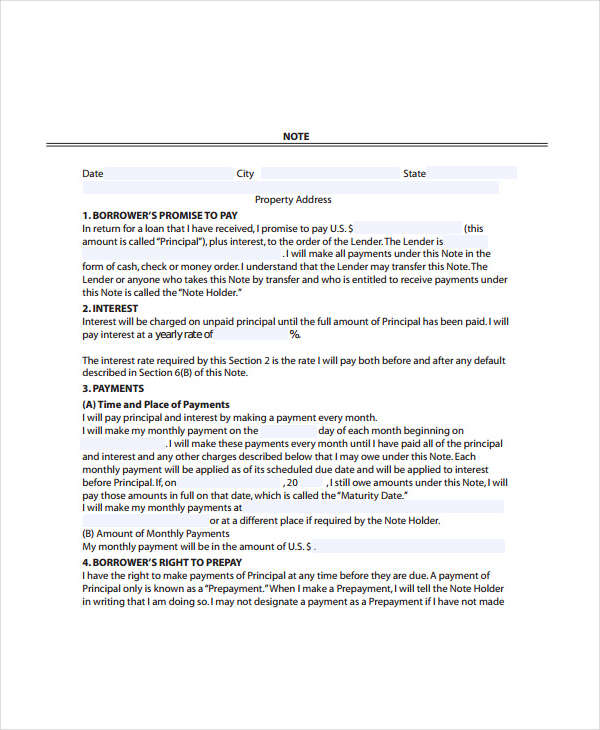

A mortgage note, often referred to as a promissory note, is a legal document that outlines the terms of a loan agreement between a borrower and a lender, secured by a mortgage. This document serves as the borrower's promise to repay the borrowed amount over a specified period, with interest. The mortgage note will typically include details such as the loan amount, interest rate, payment schedule, and any penalties for late payments or defaults. Understanding this document is crucial for both parties, as it sets the foundation for the financial transaction and ensures that both the lender and the borrower are clear about their obligations.

Components of a Sample Mortgage Note

When examining a sample mortgage note, it's important to understand its key components. These components include:

- Principal Amount: The total amount of money borrowed by the borrower.

- Interest Rate: The percentage charged by the lender for the borrowed amount.

- Repayment Schedule: The timeline and frequency of payments required to repay the loan.

- Late Payment Penalties: Fees or charges applied if the borrower fails to make payments on time.

- Default Terms: Conditions under which the borrower is considered in default of the loan agreement.

- Prepayment Clauses: Terms related to early repayment of the loan, which may include penalties or fees.

Importance of Sample Mortgage Notes

Sample mortgage notes are invaluable for several reasons. Firstly, they provide a clear and concise outline of the loan terms, ensuring that both the borrower and lender are aware of their responsibilities. This transparency helps prevent misunderstandings or disputes down the line. Additionally, a well-crafted sample mortgage note can serve as a reference for future transactions or loan modifications, making it easier to navigate changes in financial circumstances. Lastly, sample mortgage notes are a critical tool for educating new borrowers about the mortgage process, helping them make informed decisions about their financial future.

How to Draft a Sample Mortgage Note

Drafting a sample mortgage note requires careful consideration of various factors. It's essential to include all relevant details about the loan, such as the principal amount, interest rate, repayment terms, and any penalties for late payments or defaults. Additionally, the mortgage note should be written in clear and concise language, avoiding legal jargon or complex terminology that may confuse the borrower. It's also advisable to consult with a legal professional when drafting a mortgage note to ensure compliance with state and federal regulations and to address any potential legal issues that may arise.

Legal Considerations in Mortgage Notes

When drafting or reviewing a mortgage note, it's important to be aware of the legal considerations involved. This includes ensuring that the note complies with state and federal laws, such as the Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA), which require lenders to provide clear and accurate information about the loan terms. Additionally, it's crucial to address any potential legal issues related to defaults or foreclosures, as these can have significant financial and legal consequences for both the borrower and lender. Consulting with a legal professional can help ensure that the mortgage note is legally binding and enforceable, protecting the interests of both parties.

Sample Mortgage Note vs. Promissory Note

While the terms "mortgage note" and "promissory note" are often used interchangeably, there are some key differences between the two. A promissory note is a broader term that refers to any written promise to repay a loan, regardless of whether it is secured by a mortgage. In contrast, a mortgage note specifically refers to a promissory note that is secured by a mortgage on real estate. Understanding these differences is important for borrowers and lenders, as it can affect the terms of the loan agreement and the legal rights and obligations of each party.

Interest Rates and Repayment Terms

The interest rate and repayment terms outlined in a mortgage note are critical components of the loan agreement. The interest rate determines the cost of borrowing the money, while the repayment terms outline how and when the loan will be repaid. These terms can vary significantly depending on the lender, the borrower's creditworthiness, and current market conditions. It's important for borrowers to carefully review these terms before signing the mortgage note, as they will have a significant impact on the overall cost of the loan and the borrower's financial obligations.

Default Clauses and Foreclosure

Default clauses and foreclosure terms are important components of a mortgage note, as they outline the consequences of failing to meet the loan obligations. Default clauses typically specify the conditions under which the borrower is considered in default, such as missing a certain number of payments or failing to maintain adequate insurance on the property. Foreclosure terms outline the lender's rights to take possession of the property in the event of default. Understanding these terms is crucial for borrowers, as they can have significant financial and legal consequences.

Record Keeping and Documentation

Proper record keeping and documentation are essential for both borrowers and lenders when dealing with a mortgage note. This includes keeping accurate records of all payments made, any changes to the loan terms, and any correspondence between the borrower and lender. Proper documentation can help prevent disputes or misunderstandings and provide evidence in the event of a legal issue. It's also important to keep copies of the mortgage note and any related documents in a safe and secure location, as these are legally binding agreements that can have significant financial implications.

Challenges in Understanding Mortgage Notes

Despite their importance, mortgage notes can be complex and difficult to understand, especially for first-time homebuyers. Legal jargon, complex terminology, and lengthy documents can make it challenging for borrowers to fully grasp the terms of the loan agreement. To overcome these challenges, borrowers should take the time to carefully review the mortgage note, ask questions if they don't understand something, and seek professional advice if necessary. Understanding the mortgage note is crucial for making informed financial decisions and avoiding potential legal and financial issues down the line.

Frequently Asked Questions

- What is the purpose of a mortgage note?

The purpose of a mortgage note is to outline the terms of a loan agreement between a borrower and a lender, secured by a mortgage. It serves as a legally binding document that specifies the borrower's promise to repay the loan over a specified period.

- Can a mortgage note be transferred?

Yes, a mortgage note can be transferred or sold to another party. This is a common practice in the mortgage industry, and it means that the new owner of the note becomes the lender, and the borrower must make payments to them.

- What happens if I default on my mortgage note?

If you default on your mortgage note, the lender has the legal right to initiate foreclosure proceedings, which can result in the loss of your home. It's important to understand the default terms in your mortgage note and to communicate with your lender if you're having trouble making payments.

- Can I modify the terms of my mortgage note?

In some cases, it may be possible to modify the terms of your mortgage note, such as extending the repayment period or changing the interest rate. This typically requires negotiating with your lender and may involve additional fees or conditions.

- How can I ensure that my mortgage note is legally binding?

To ensure that your mortgage note is legally binding, it's important to have it reviewed by a legal professional and to ensure that it complies with all applicable state and federal laws. Additionally, both parties should sign the document, and it should be properly notarized and recorded.

- Where can I find a sample mortgage note?

Sample mortgage notes are available from various sources, including online legal document providers, real estate professionals, and financial institutions. It's important to ensure that any sample mortgage note you use is tailored to your specific needs and complies with relevant laws.

Conclusion

In conclusion, understanding and utilizing a sample mortgage note is a critical step in any real estate transaction. It provides a clear and concise outline of the loan terms, ensuring that both the borrower and lender are aware of their responsibilities and rights. By taking the time to carefully review and understand the mortgage note, borrowers can make informed financial decisions and avoid potential legal and financial issues down the line. Whether you're a first-time homebuyer or an experienced real estate professional, having a solid understanding of mortgage notes is essential for navigating the complex world of real estate finance.

For further information, readers can visit Consumer Financial Protection Bureau, a resourceful site containing comprehensive information on mortgage notes and related financial documents.

You Might Also Like

Insights Into The Life And Achievements Of Robert A. MinicucciDrug Test Protocols For Firefighters: Ensuring Safety And Reliability

Cedric Richmond Net Worth: Insights And Analysis

Fulcrum LNG: Innovation And Sustainability In The Energy Sector

David Kaye Real Estate: A Comprehensive Guide To Success In Property Investment

Article Recommendations

- James Cook Practice This Week Latest Updates

- Young Jeezys Net Worth Inside The Financial Success Of A Hiphop Icon

- Espns Beth Mowins Highlights News