The intricacies of mortgage agreements can often be daunting for homeowners, especially when it comes to understanding specific clauses like the due on sale clause. This clause, often buried within the fine print, can have significant implications for those looking to sell or transfer their property. Understanding the due on sale clause in a mortgage is crucial for homeowners who wish to avoid potential pitfalls and ensure a smooth transaction process. This guide aims to demystify this clause and provide practical insights for navigating its complexities.

In essence, the due on sale clause in a mortgage is a provision that allows the lender to demand the full repayment of the remaining loan balance upon the sale or transfer of the property. While it serves as a protective measure for lenders, ensuring that they receive full compensation for the loan, it can pose challenges for property owners who are unaware of its existence or implications. This clause can affect refinancing options, property transfers to family members, and even sales in certain markets.

For homeowners planning any changes in property ownership, whether through sale, inheritance, or other means, it is imperative to have a comprehensive understanding of the due on sale clause in their mortgage. This article provides an in-depth exploration of the clause, outlining its purpose, function, and potential impact on homeowners. Through this guide, readers will gain valuable knowledge and strategies to handle this clause effectively, ensuring informed decision-making and the protection of their financial interests.

Table of Contents

- What is the Due on Sale Clause?

- Historical Background of the Due on Sale Clause

- Purpose and Importance of the Clause

- Legal Framework and Regulations

- How It Affects Homeowners

- Exemptions and Exceptions

- Strategies to Navigate the Clause

- Impact on the Real Estate Market

- Case Studies: Real-Life Implications

- The Role of Lenders

- Alternatives to the Due on Sale Clause

- Future Trends and Developments

- Common Misconceptions and Myths

- Frequently Asked Questions

- Conclusion

What is the Due on Sale Clause?

The due on sale clause, often included in mortgage agreements, is a stipulation that empowers the lender to demand full repayment of the outstanding loan balance when the property is sold or transferred. This clause ensures that the lender can protect its interest in the loan by preventing unauthorized transfers that might alter the risk profile of the borrower. Essentially, it acts as a safeguard for lenders, allowing them to reassess the loan terms or demand payment in full whenever the property changes hands.

While the clause primarily serves to protect the lender, it also has significant implications for homeowners. For instance, if a homeowner wishes to sell their property, the presence of a due on sale clause means that the new buyer cannot assume the existing mortgage. Instead, the seller must settle the outstanding loan amount before transferring ownership. This requirement can impact the seller's ability to attract buyers, particularly in regions where mortgage interest rates are volatile.

Moreover, the due on sale clause can affect situations where a property is transferred to a family member, such as through inheritance or a gift. In these cases, the lender retains the right to invoke the clause, demanding repayment of the mortgage balance. Understanding the full scope of this clause is essential for homeowners to effectively manage their property transactions and avoid unexpected financial liabilities.

Historical Background of the Due on Sale Clause

The due on sale clause has a storied history, rooted in the evolving landscape of the mortgage industry. Originally introduced as a tool for lenders to control the risk associated with property transfers, the clause gained prominence in the mid-20th century. During this period, the housing market experienced rapid growth, prompting lenders to seek mechanisms that would allow them to maintain control over loan agreements despite changes in property ownership.

One of the major turning points in the history of the due on sale clause was the landmark court case of "Garn-St. Germain Depository Institutions Act of 1982." This legislation was pivotal in clarifying the scope and enforceability of the clause, ultimately granting lenders the authority to enforce it more broadly. As a result, the due on sale clause became a standard feature in most mortgage agreements, reflecting its importance as a protective measure for lenders.

Over the years, the due on sale clause has been shaped by various legal precedents and regulatory changes. As the mortgage industry continues to evolve, the clause remains a key element of mortgage agreements, underscoring its enduring significance in safeguarding lender interests while balancing the rights of homeowners.

Purpose and Importance of the Clause

The primary purpose of the due on sale clause is to protect lenders from the risks associated with unauthorized transfers of property ownership. By allowing lenders to demand full repayment of the mortgage when a property is sold or transferred, the clause ensures that lenders maintain control over the loan terms and conditions. This control is crucial in mitigating the financial risks that arise when borrowers transfer their property to parties who may not meet the original lending criteria.

Additionally, the due on sale clause plays a vital role in preserving the lender's investment in the property. It prevents borrowers from transferring the mortgage to another party without the lender's consent, thereby ensuring that the lender's risk exposure remains consistent with the original loan agreement. This is particularly important in scenarios where interest rates have risen since the mortgage was issued, as it allows lenders to adjust the terms of the loan to reflect the current market conditions.

For homeowners, understanding the due on sale clause is essential for effective property management and financial planning. By being aware of the clause's implications, homeowners can make informed decisions about selling or transferring their property, while also exploring potential strategies to navigate the clause's requirements. Ultimately, the due on sale clause serves as a crucial element of mortgage agreements, balancing the interests of both lenders and borrowers.

Legal Framework and Regulations

The legal framework surrounding the due on sale clause is governed by a combination of federal and state regulations. At the federal level, the Garn-St. Germain Depository Institutions Act of 1982 is the primary legislation that defines the enforceability of the clause. This act grants lenders the authority to include due on sale clauses in mortgage agreements and outlines specific circumstances under which the clause can be invoked.

Under the Garn-St. Germain Act, lenders are prohibited from enforcing the due on sale clause in certain situations, such as when the property is transferred to a spouse as part of a divorce settlement or when the property is inherited by a relative. These exemptions are designed to balance the interests of lenders with the rights of homeowners, ensuring that the clause is not used to unfairly disadvantage borrowers in specific scenarios.

In addition to federal regulations, state laws may also impact the enforceability of the due on sale clause. Some states have enacted legislation that provides additional protections for homeowners, limiting the circumstances under which lenders can demand full repayment of the mortgage. Homeowners should familiarize themselves with the legal framework in their jurisdiction to understand how the due on sale clause may apply to their specific situation.

How It Affects Homeowners

The due on sale clause can have significant implications for homeowners, particularly when it comes to selling or transferring their property. One of the most direct effects of the clause is its impact on the ability to transfer the mortgage to a new buyer. In most cases, the clause requires the full repayment of the existing mortgage before the property can be sold or transferred, which can limit the options available to homeowners.

For homeowners looking to sell their property, the due on sale clause can affect the attractiveness of the home to potential buyers. If the clause is enforced, buyers may be unable to assume the existing mortgage, which could limit their financing options or result in higher interest rates. This can be particularly challenging in markets where interest rates have risen since the original mortgage was issued, making it more expensive for buyers to obtain new financing.

Additionally, the due on sale clause can impact property transfers within families. For example, if a homeowner wishes to transfer their property to a child or other family member, the lender may require full repayment of the mortgage before the transfer can occur. This can create financial challenges for families who are not prepared to pay off the remaining loan balance, potentially leading to the sale of the property or other financial arrangements.

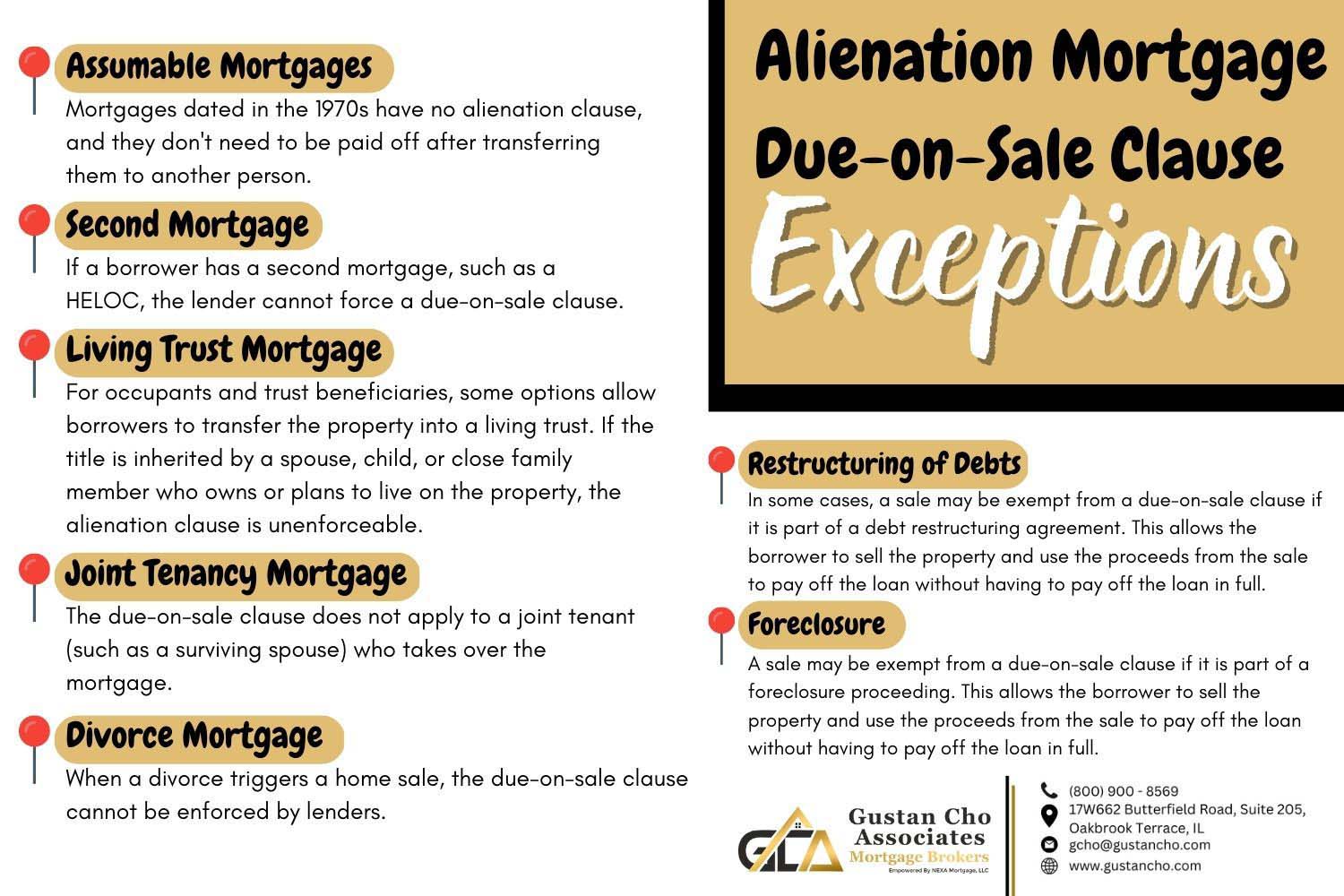

Exemptions and Exceptions

While the due on sale clause is a powerful tool for lenders, there are several exemptions and exceptions that protect homeowners in certain situations. Under federal law, there are specific scenarios where lenders are prohibited from enforcing the clause, providing homeowners with greater flexibility in managing their property transfers.

One common exemption is for transfers between spouses. If a property is transferred to a spouse as part of a divorce settlement, the lender cannot enforce the due on sale clause. This exemption ensures that homeowners can make necessary adjustments to property ownership without facing financial penalties.

Another exemption applies to property transfers resulting from the death of a borrower. If a property is inherited by a relative, the lender is prohibited from demanding full repayment of the mortgage. This provision provides families with the opportunity to retain ownership of the property without the immediate financial burden of repaying the loan.

In addition to these federal exemptions, some states have enacted additional protections for homeowners. These state-level regulations may provide further exceptions to the due on sale clause, ensuring that homeowners have the flexibility to manage their property transfers without undue financial hardship. Homeowners should consult with legal professionals to understand the specific exemptions and exceptions that may apply to their situation.

Strategies to Navigate the Clause

For homeowners looking to navigate the complexities of the due on sale clause, there are several strategies that can help manage its implications effectively. One approach is to negotiate with the lender for an assumption of the mortgage, allowing the new buyer to take over the existing loan. While not all lenders may agree to this arrangement, it can be a viable option for those looking to facilitate a property transfer without triggering the clause.

Another strategy is to explore the possibility of refinancing the mortgage. By refinancing, homeowners can replace the existing loan with a new one, potentially securing more favorable terms and avoiding the due on sale clause altogether. This option may be particularly advantageous in markets where interest rates have decreased since the original mortgage was issued.

- Assumption of Mortgage: Negotiate with the lender to allow the new buyer to assume the existing mortgage, avoiding the due on sale clause.

- Refinancing: Consider refinancing the mortgage to secure better terms and eliminate the clause's impact on property transfers.

- Consult Legal Advice: Seek guidance from legal professionals to understand the full implications of the clause and identify potential exemptions.

Impact on the Real Estate Market

The due on sale clause has a significant impact on the real estate market, influencing both the behavior of buyers and sellers as well as the overall dynamics of property transactions. For sellers, the presence of the clause can affect the marketability of their property, particularly if interest rates have risen since the original mortgage was issued. In such cases, potential buyers may face higher financing costs, making it more challenging to attract offers.

For buyers, the due on sale clause can limit their options when it comes to financing a property purchase. If the clause is enforced, buyers may be unable to assume the existing mortgage, which could result in higher interest rates or reduced borrowing capacity. This can impact the affordability of homes and influence buyer behavior, potentially leading to a slowdown in property sales.

Overall, the due on sale clause plays a critical role in shaping the real estate market, affecting both individual transactions and broader market trends. By understanding its implications, buyers and sellers can make informed decisions and navigate the complexities of property transactions with confidence.

Case Studies: Real-Life Implications

To illustrate the real-life implications of the due on sale clause, consider the following case studies:

- A homeowner in a rising interest rate environment wishes to sell their property. The potential buyer is interested in assuming the existing mortgage, which has a lower interest rate than current market offerings. However, the due on sale clause is enforced, requiring the seller to pay off the mortgage in full before the transfer. As a result, the buyer is unable to assume the mortgage, leading to a renegotiation of the sale terms.

- A family inherits a property from a deceased relative. The mortgage on the property includes a due on sale clause, but federal law exempts the lender from enforcing it in this scenario. The family is able to retain ownership of the property without the immediate need to repay the mortgage, allowing them to manage the estate according to their preferences.

- A couple undergoing a divorce agrees to transfer the property to one spouse as part of the settlement. Despite the presence of a due on sale clause, the lender is prohibited from enforcing it under federal law. The transfer proceeds smoothly, allowing both parties to move forward with their respective financial plans.

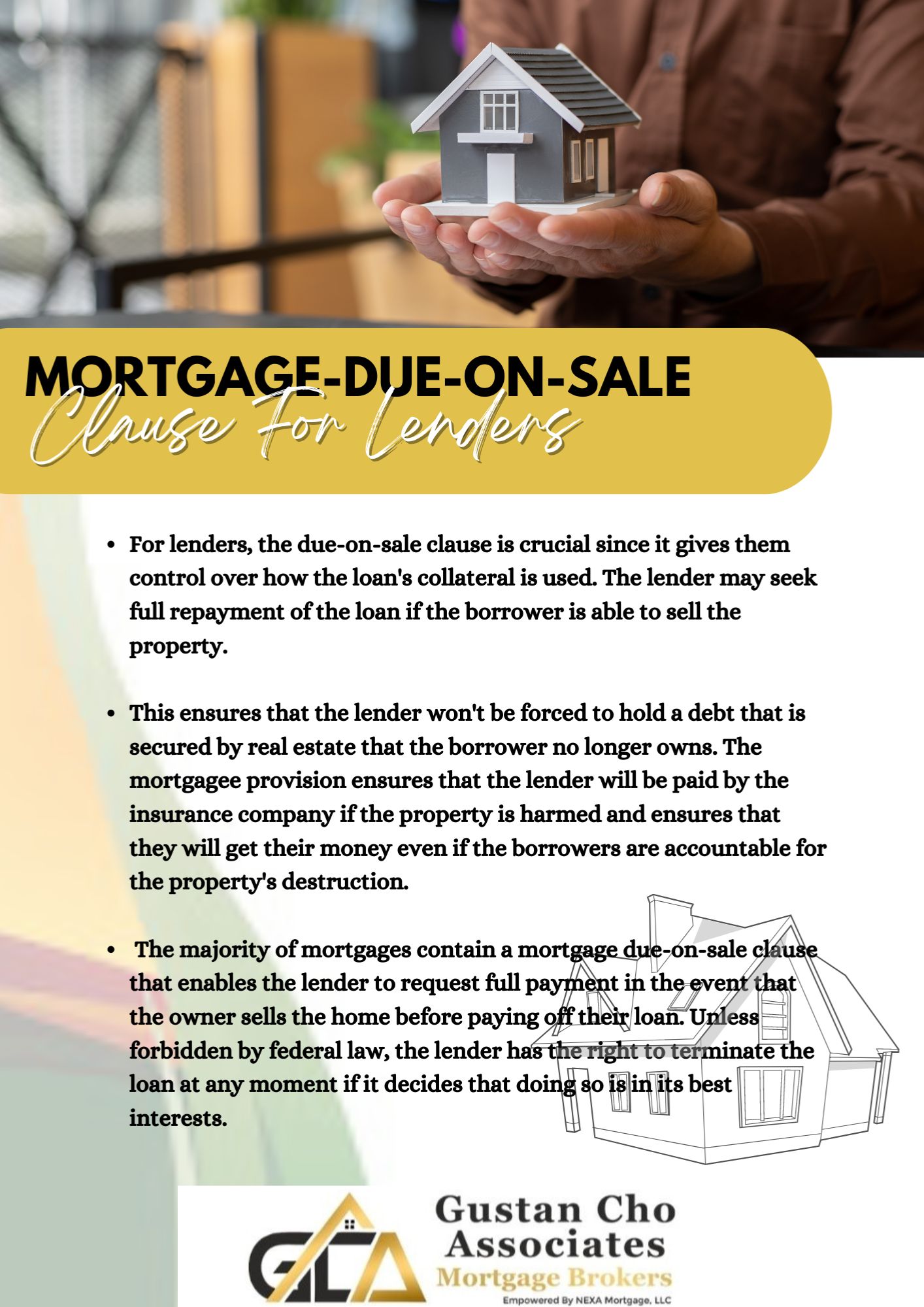

The Role of Lenders

Lenders play a crucial role in the enforcement and management of the due on sale clause. As the primary stakeholders in mortgage agreements, lenders have the authority to determine whether to enforce the clause and under what circumstances. This decision is often influenced by factors such as the borrower's creditworthiness, the property's market value, and the prevailing interest rate environment.

In some cases, lenders may choose to waive the due on sale clause or negotiate alternative arrangements with borrowers. This flexibility can be beneficial for both parties, allowing lenders to maintain a positive relationship with borrowers while also protecting their financial interests. However, the decision to waive the clause is typically made on a case-by-case basis, taking into account the specific circumstances of the property transfer.

Ultimately, lenders have a vested interest in ensuring that mortgage agreements are honored and that their financial exposure is managed effectively. By understanding the lender's perspective, homeowners can better navigate the due on sale clause and explore potential solutions that align with their financial goals.

Alternatives to the Due on Sale Clause

While the due on sale clause is a common feature in mortgage agreements, there are alternative approaches that can provide greater flexibility for homeowners and lenders alike. One such alternative is the inclusion of a "transfer on death" clause, which allows for the seamless transfer of property ownership upon the death of the borrower without triggering the due on sale clause.

Another option is the use of a "wraparound mortgage," which allows the buyer to assume the existing mortgage while also taking on additional financing. This approach can be beneficial in situations where interest rates have risen since the original mortgage was issued, providing the buyer with more favorable loan terms while also accommodating the seller's needs.

By exploring these and other alternatives, homeowners can identify strategies that align with their financial goals and facilitate property transfers without the constraints of the due on sale clause. It is essential for homeowners to work closely with lenders and legal professionals to ensure that any alternative arrangements are legally sound and financially viable.

Future Trends and Developments

As the mortgage industry continues to evolve, the due on sale clause is likely to undergo further developments and adaptations. One potential trend is the increasing use of technology to streamline mortgage agreements and enhance transparency for borrowers. This could include the use of digital platforms to provide real-time updates on mortgage terms and conditions, empowering homeowners to make informed decisions about property transfers.

Another potential trend is the growing emphasis on sustainability and green financing options. As lenders seek to align their offerings with environmental goals, there may be opportunities to incorporate sustainable practices into mortgage agreements, including alternative approaches to the due on sale clause.

Overall, the future of the due on sale clause will be shaped by a combination of technological advancements, regulatory changes, and shifts in consumer preferences. Homeowners and lenders alike must stay informed about these trends to navigate the evolving landscape of mortgage agreements effectively.

Common Misconceptions and Myths

There are several common misconceptions and myths surrounding the due on sale clause that can lead to confusion for homeowners. One such myth is that the clause is automatically enforced in all property transfers. In reality, the enforceability of the clause depends on various factors, including the specific terms of the mortgage agreement and applicable legal exemptions.

Another misconception is that the due on sale clause prevents any transfer of property ownership. While the clause does impose certain restrictions, there are exemptions and alternatives that allow for property transfers under specific circumstances.

By dispelling these myths and gaining a clear understanding of the due on sale clause, homeowners can make informed decisions about their property transactions and avoid potential pitfalls. It is essential for homeowners to seek guidance from legal and financial professionals to ensure that they fully understand the implications of the clause and their options for navigating it.

Frequently Asked Questions

- What is the due on sale clause in a mortgage?

The due on sale clause is a provision in a mortgage agreement that allows the lender to demand full repayment of the loan balance when the property is sold or transferred.

- Can the due on sale clause be waived?

In some cases, lenders may choose to waive the due on sale clause or negotiate alternative arrangements with borrowers, depending on the specific circumstances of the property transfer.

- Are there exemptions to the due on sale clause?

Yes, federal law provides specific exemptions where the clause cannot be enforced, such as in transfers between spouses or when a property is inherited by a relative.

- How does the due on sale clause affect property transfers within families?

The clause can impact family transfers by requiring full repayment of the mortgage unless exemptions apply, potentially leading to financial challenges for families.

- What are some alternatives to the due on sale clause?

Alternatives include transfer on death clauses and wraparound mortgages, which provide greater flexibility for property transfers without triggering the due on sale clause.

- How can homeowners navigate the due on sale clause effectively?

Homeowners can explore options such as mortgage assumptions, refinancing, and consulting legal professionals to manage the implications of the clause effectively.

Conclusion

The due on sale clause in a mortgage represents a critical element of property ownership and financing, impacting both homeowners and lenders in significant ways. By understanding the purpose, implications, and strategies for navigating this clause, homeowners can make informed decisions about their property transactions and safeguard their financial interests.

As the real estate market and mortgage industry continue to evolve, staying informed about the latest trends and developments will be essential for homeowners to navigate the complexities of mortgage agreements effectively. By working closely with lenders and legal professionals, homeowners can explore alternatives and exemptions that align with their financial goals, ensuring a smooth and successful property transfer process.

Ultimately, the due on sale clause serves as a valuable tool for balancing the interests of both lenders and borrowers, providing a framework for managing property transfers while protecting the financial stability of all parties involved. With the right knowledge and strategies, homeowners can confidently navigate this clause and achieve their property ownership objectives.

You Might Also Like

Vitality Botanicals Kratom Supply: Essential Insights And BenefitsMastering Nvidia Volatility: A Guide To Understanding Market Dynamics

Unrivaled Messi AI: Revolutionizing The Future Of Football

The Future Of Wellness: Ayr Wellness Gainesville's Impact On The Community

The Remarkable Life And Achievements Of Brett Jenkins: A Comprehensive Overview

Article Recommendations

- Mitch Mcconnells Hands Health Concerns Explained

- Senator Ted Cruzs Revelation Exposing Mitch Mcconnells Political Maneuvers

- Understanding Iga Swiateks Partner A Detailed Insight Into Her Life