Navigating the landscape of investment opportunities can be daunting, especially when faced with financial jargon that seems complex at first glance. However, by breaking down these terms into understandable elements, anyone can become well-versed in the essentials of investing. The dividend rate and APY CD are both vital components of financial literacy, offering unique benefits depending on an individual's investment style and objectives. With a focus on clarity and practical insights, this guide aims to demystify these terms, offering readers the tools to achieve success in their financial endeavors. For those seeking to diversify their portfolios or simply enhance their returns on savings, understanding the distinctions between dividend rates and APY CDs is a step in the right direction. This article serves as a resource for seasoned investors and newcomers alike, exploring the intricacies of each term and the scenarios in which they thrive. By the end, readers will be equipped with the knowledge needed to make strategic choices that bolster their financial well-being.

Understanding Dividend Rate

The dividend rate is a financial term that refers to the amount of money a company pays to its shareholders out of its profits, usually on a quarterly basis. It is expressed as a percentage of the stock's current price. Dividend rates are an essential component of an investor's total return and are often used as an indicator of a company's financial health. Companies that consistently pay dividends are generally considered stable and reliable, making them attractive to conservative investors.

To calculate the dividend rate, you simply divide the annual dividend payment by the stock's current price. This gives you a percentage that represents the yield of the stock based on its current price. For example, if a company pays an annual dividend of $2 per share and the stock is priced at $50, the dividend rate would be 4%.

Investors often seek out stocks with high dividend rates as they provide a steady income stream, which can be particularly appealing during periods of market volatility when capital gains are less predictable. Additionally, dividends can be reinvested to purchase more shares, compounding the investor's returns over time.

Dividend rates can vary widely between industries and companies. Some sectors, such as utilities and real estate investment trusts (REITs), are known for offering higher dividend rates due to their stable cash flows and regulatory requirements. On the other hand, growth-oriented sectors like technology may offer lower dividend rates as they prefer to reinvest profits into business expansion.

It's important to note that a high dividend rate does not necessarily indicate a good investment. Investors should also consider the company's dividend history, payout ratio, and overall financial health. A company with a high dividend rate but a poor financial outlook may not be able to sustain its dividend payments, leading to potential losses for investors.

Exploring APY CD

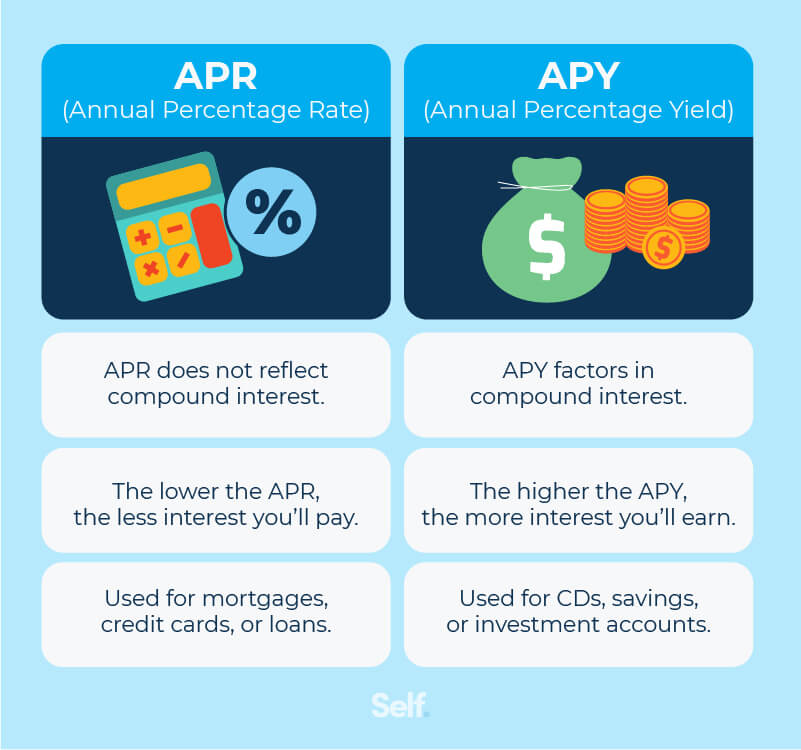

Annual Percentage Yield (APY) is a metric used to measure the real rate of return on an investment, taking into account the effect of compounding interest. A Certificate of Deposit (CD) is a type of savings account offered by banks and credit unions, typically with a fixed interest rate and maturity date. The combination of APY and CD is a popular savings vehicle for individuals seeking a low-risk investment with predictable returns.

APY CD accounts are particularly attractive to conservative investors who prioritize capital preservation and steady income over high-risk, high-reward opportunities. CDs generally offer higher interest rates than regular savings accounts, especially when the funds are locked in for a longer term. The fixed rate of return provides certainty, allowing investors to plan their finances with confidence.

The APY is calculated by taking the nominal interest rate and factoring in the effect of compounding, which can occur on a daily, monthly, or quarterly basis. The more frequent the compounding, the higher the APY will be. This makes APY a more accurate representation of the investment's earning potential compared to simple interest rates.

When choosing an APY CD, investors need to consider the term length, interest rate, and penalties for early withdrawal. Longer-term CDs usually offer higher interest rates, but they also require the investor to lock in their funds for extended periods. Early withdrawal can result in significant penalties, reducing the overall return on investment.

APY CDs are considered low-risk investments as they are typically insured by the FDIC (Federal Deposit Insurance Corporation) or NCUA (National Credit Union Administration) for amounts up to $250,000 per depositor, per institution. This insurance protects the investor's principal and interest in the event of a bank failure.

Key Differences Between Dividend Rate and APY CD

The primary difference between dividend rates and APY CDs lies in their nature and application. Dividend rates pertain to stocks and represent the cash income received from owning shares in a company. They are subject to market fluctuations and the financial performance of the issuing company. On the other hand, APY CDs are fixed-income investment products offered by financial institutions, providing a guaranteed rate of return over a specified term.

Another significant difference is the risk profile associated with each option. Dividend rates are inherently riskier due to their reliance on the company's profitability and market conditions. Share prices can fluctuate, impacting the total return on investment. Conversely, APY CDs are low-risk investments with predictable returns, offering stability and security for conservative investors.

Liquidity is another factor that distinguishes dividend rates from APY CDs. Stocks with dividend rates can be bought and sold on the open market, offering greater flexibility and liquidity. However, APY CDs require the investor to commit their funds for a set period, with penalties for early withdrawal, limiting liquidity.

Finally, tax implications differ between the two investment options. Dividends are typically taxed at a lower rate as qualified dividends, while interest earned from APY CDs is taxed as ordinary income. Investors should consider the tax implications when choosing between dividend rates and APY CDs to optimize their after-tax returns.

Advantages of Dividend Rates

Dividend rates offer several advantages to investors, particularly those seeking income-generating investments. One of the primary benefits is the potential for regular income. Companies that pay dividends provide shareholders with a steady cash flow, which can be reinvested or used to supplement income during retirement.

The reinvestment of dividends can lead to compounding returns over time, enhancing the investor's overall financial growth. By purchasing additional shares with dividend payments, investors can increase their ownership in the company and potentially benefit from capital appreciation as well.

Dividend-paying stocks are often perceived as less volatile compared to their non-dividend counterparts. Companies that consistently pay dividends are typically well-established and financially stable, providing a degree of protection against market downturns. This stability can be particularly appealing to risk-averse investors.

Furthermore, dividend-paying stocks may offer a hedge against inflation. As companies grow and increase their profits, they may raise dividend payments, providing investors with a rising income stream that helps maintain purchasing power in an inflationary environment.

Finally, the tax treatment of dividends can be advantageous for investors. Qualified dividends are taxed at a lower rate compared to ordinary income, allowing investors to retain more of their earnings. This favorable tax treatment can enhance the overall return on investment.

Advantages of APY CDs

APY CDs are considered one of the safest investment options, providing a predictable and secure return on investment. The fixed interest rate offered by CDs ensures that investors know exactly how much they will earn over the term, allowing for effective financial planning.

The insurance provided by the FDIC or NCUA further enhances the safety of APY CDs, protecting investors' principal and interest up to $250,000 per depositor, per institution. This insurance coverage provides peace of mind and security, particularly important for conservative investors focused on capital preservation.

APY CDs offer higher interest rates compared to traditional savings accounts, making them an attractive option for investors seeking better returns without taking on excessive risk. The higher rates are particularly beneficial when interest rates in the economy are low, providing a reliable source of income.

The lack of market volatility associated with APY CDs is another advantage, as the return is not influenced by market fluctuations or economic downturns. This stability makes APY CDs appealing to risk-averse individuals who prefer certainty over potential capital gains.

Additionally, APY CDs can be laddered to provide a balance between liquidity and return. By staggering the maturity dates of multiple CDs, investors can access their funds at regular intervals while still benefiting from higher interest rates on longer-term investments.

Risks Associated with Dividend Rates

While dividend rates offer several advantages, they also come with inherent risks. The primary risk is the potential for dividend cuts or suspensions if the company experiences financial difficulties. A reduction or elimination of dividends can significantly impact an investor's income and total return.

Market volatility is another risk associated with dividend rates. Stock prices can fluctuate based on various factors, including economic conditions, industry trends, and company performance. These fluctuations can affect the value of an investor's holdings and the overall return on investment.

Dividend-paying stocks are often concentrated in specific sectors, such as utilities, consumer staples, and financials. This concentration can expose investors to sector-specific risks, such as regulatory changes, technological advancements, or shifts in consumer preferences. Diversification is essential to mitigate these risks.

Additionally, dividend rates are not guaranteed, and companies may choose to reduce or eliminate dividends to reinvest profits into growth initiatives. This can be disappointing for investors relying on dividends for income, emphasizing the importance of evaluating a company's financial health and dividend history before investing.

Finally, the tax treatment of dividends can impact an investor's after-tax return. While qualified dividends benefit from lower tax rates, non-qualified dividends are taxed as ordinary income, potentially reducing the overall return on investment.

Risks Associated with APY CDs

Despite their safety, APY CDs also present certain risks. One of the primary risks is the opportunity cost associated with locking in funds for a fixed term. If interest rates rise during the term, investors may miss out on higher returns available from other investment options.

Early withdrawal penalties are another risk, as accessing funds before the maturity date can result in significant penalties, reducing the overall return on investment. Investors should carefully consider their liquidity needs before committing to a long-term CD.

Inflation is a potential risk for APY CDs, as the fixed interest rate may not keep pace with rising prices. This can erode the purchasing power of the investment over time, particularly during periods of high inflation.

APY CDs also lack the potential for capital appreciation, limiting the overall growth potential of the investment. While they offer stability and predictability, investors seeking higher returns may need to consider other investment options with greater growth prospects.

Finally, reinvestment risk is a concern for APY CD investors. As CDs mature, investors may need to reinvest the principal at lower interest rates if market conditions have changed. This can impact the overall return and necessitate adjustments to the investment strategy.

Dividend Rate vs APY CD: Which to Choose?

The decision between dividend rates and APY CDs ultimately depends on an individual's financial goals, risk tolerance, and investment horizon. Dividend rates are suitable for investors seeking income-generating investments with the potential for capital appreciation. They offer a higher degree of risk and volatility but can provide significant returns over time, particularly when dividends are reinvested.

On the other hand, APY CDs are ideal for conservative investors prioritizing capital preservation and predictable income. They offer safety and stability, making them suitable for individuals nearing retirement or those with a low-risk tolerance. However, the potential for growth is limited, and the fixed rate of return may not keep pace with inflation.

Investors may also consider a combination of dividend-paying stocks and APY CDs to balance risk and return in their portfolios. This approach allows for diversification, providing both income and growth potential while mitigating the risks associated with each investment type.

Ultimately, the choice between dividend rates and APY CDs should align with an individual's broader financial strategy, taking into account factors such as investment objectives, time horizon, and risk tolerance. Consultation with a financial advisor can provide personalized guidance and support in making informed investment decisions.

How to Calculate Dividend Rates

Calculating the dividend rate involves determining the annual dividend payment and dividing it by the stock's current price. This calculation provides a percentage that represents the yield of the stock based on its current price. Here is a step-by-step guide to calculating dividend rates:

- Determine the annual dividend payment: This information is typically available on the company's investor relations website or financial statements. Annual dividend payments are usually expressed on a per-share basis.

- Find the stock's current price: The current price can be obtained from financial news websites, stock market apps, or your brokerage account. It represents the most recent trading price of the stock.

- Divide the annual dividend payment by the stock's current price: This calculation provides the dividend yield, expressed as a percentage.

For example, if a company pays an annual dividend of $3 per share and the stock is priced at $60, the dividend rate would be:

Dividend Rate = ($3 / $60) * 100 = 5%

This 5% yield indicates the return an investor can expect from the dividend payments relative to the stock's current price.

How to Calculate APY

Calculating APY involves accounting for the effect of compounding interest on the nominal interest rate. The formula for calculating APY is:

APY = (1 + r/n)n - 1

- r represents the nominal interest rate (expressed as a decimal).

- n represents the number of compounding periods per year.

Here is a step-by-step guide to calculating APY:

- Determine the nominal interest rate: This is the stated annual interest rate of the investment.

- Identify the number of compounding periods: Common compounding frequencies include daily, monthly, or quarterly.

- Plug the values into the formula and calculate APY.

For example, if a CD offers a nominal interest rate of 4% with quarterly compounding, the APY would be calculated as follows:

APY = (1 + 0.04/4)4 - 1 = 0.0406 or 4.06%

This 4.06% APY reflects the investment's real rate of return, accounting for the effect of compounding interest.

Impact of Economic Factors on Dividend Rates and APY CDs

Economic factors play a significant role in influencing both dividend rates and APY CDs. Understanding these factors can help investors make informed decisions and anticipate potential changes in their investment returns.

Interest rates are a key economic factor affecting both dividend rates and APY CDs. When interest rates rise, companies may face higher borrowing costs, potentially impacting their profitability and ability to pay dividends. Conversely, higher interest rates often lead to increased APY CD rates, offering better returns for investors.

Economic growth and inflation are also important considerations. During periods of economic expansion, companies may increase dividends due to rising profits, while APY CD rates may remain stable or increase. Inflation can erode the purchasing power of fixed-income investments like APY CDs, making dividend-paying stocks more appealing as they may offer a rising income stream.

Market volatility can impact dividend rates, as fluctuations in stock prices affect the yield relative to the investment's value. Investors may seek safety in APY CDs during volatile market conditions, as they provide a stable return regardless of market fluctuations.

Regulatory and fiscal policies can also influence dividend rates and APY CDs. Changes in tax laws, interest rate policies, and government spending can impact company profitability and interest rates, affecting the returns on both investment options.

Real-World Examples of Dividend Rates and APY CDs

To illustrate the concepts of dividend rates and APY CDs, let's explore some real-world examples.

One well-known company that pays dividends is The Coca-Cola Company. As of the latest financial statements, Coca-Cola pays an annual dividend of $1.68 per share. With a stock price of $54, the dividend rate would be approximately 3.1%. This indicates the yield investors can expect from holding Coca-Cola shares, making it an attractive option for income-seeking investors.

On the APY CD side, consider a one-year CD offered by a major bank with a nominal interest rate of 2.5% and monthly compounding. Using the APY formula, the real rate of return would be approximately 2.53%. This fixed return provides a secure and predictable income stream for investors seeking stability.

These examples highlight the different characteristics and benefits of dividend rates and APY CDs, helping investors understand the potential returns and risks associated with each option.

Common Misconceptions About Dividend Rates and APY CDs

Several misconceptions surround dividend rates and APY CDs, leading to confusion among investors. Addressing these misconceptions can help investors make more informed decisions.

One common misconception is that a high dividend rate always indicates a good investment. While high dividend rates can be attractive, they may also signal potential financial instability or unsustainable payouts. Investors should evaluate the company's financial health and dividend history before investing.

Another misconception is that APY CDs are risk-free investments. While they are considered low-risk, they are not entirely risk-free. Factors such as inflation, interest rate changes, and early withdrawal penalties can impact the overall return on investment.

Some investors believe that dividend-paying stocks are inherently safer than non-dividend stocks. While they may offer stability, dividend-paying stocks are not immune to market fluctuations or company-specific risks. Diversification is essential to mitigate these risks.

Lastly, some investors assume that APY CDs are only suitable for retirees or conservative investors. While they are popular among these groups, APY CDs can also be a valuable component of a diversified portfolio for investors seeking stability and predictable returns.

Frequently Asked Questions

1. What is the difference between a dividend rate and an APY CD?

The dividend rate pertains to the cash income received from owning shares in a company, expressed as a percentage of the stock's current price. APY CD refers to a fixed-income investment product offered by financial institutions, providing a guaranteed rate of return over a specified term.

2. How are dividend rates calculated?

Dividend rates are calculated by dividing the annual dividend payment by the stock's current price, expressed as a percentage. This yield represents the return an investor can expect from dividend payments relative to the stock's price.

3. What does APY mean, and how is it calculated?

APY (Annual Percentage Yield) accounts for the effect of compounding interest on the nominal interest rate. It is calculated using the formula: APY = (1 + r/n)n - 1, where r is the nominal interest rate and n is the number of compounding periods per year.

4. Are dividend rates or APY CDs better for retirement planning?

Both dividend rates and APY CDs can be suitable for retirement planning, depending on an individual's financial goals and risk tolerance. Dividend rates offer potential income and growth, while APY CDs provide stability and predictable returns.

5. Can I lose money with dividend-paying stocks?

Yes, dividend-paying stocks are subject to market fluctuations and company-specific risks, which can affect the value of your investment. It's essential to diversify your portfolio to mitigate these risks.

6. Are APY CDs risk-free?

APY CDs are considered low-risk investments, but they are not entirely risk-free. Factors such as inflation, interest rate changes, and early withdrawal penalties can impact the overall return on investment.

Conclusion

In the realm of personal finance, understanding the nuances of dividend rates and APY CDs is essential for making informed investment decisions. Both options offer unique benefits and cater to different financial strategies. Dividend rates provide the potential for income and growth, appealing to investors seeking higher returns with a degree of risk. Conversely, APY CDs offer stability and predictable returns, making them suitable for conservative investors prioritizing capital preservation.

The choice between dividend rates and APY CDs should align with an individual's financial goals, risk tolerance, and investment horizon. Diversification can balance the risks and returns of each option, optimizing the overall investment strategy. By understanding the key differences, advantages, and risks associated with dividend rates and APY CDs, investors can make confident decisions that enhance their financial well-being.

For additional resources and insights on personal finance and investment strategies, consider visiting [Investopedia](https://www.investopedia.com) for expert advice and guidance.

You Might Also Like

Integra Trading: Your Guide To Success In The Trading WorldCircle K Exit 22: An In-Depth Guide To Your Next Stop

Georgia Dream Peach Plus: A Path To Homeownership Success

Essential Guide To Cres Home Warranty Services

Understanding The Saint Gaudens Double Eagle Value: A Numismatic Treasure

Article Recommendations

- Mitch Mcconnells Role In Obamas Presidency A Oneterm Fate

- Mitch Mcconnell Minority Leader When

- Tragic News Pentatonix Member Dies Unexpectedly

:max_bytes(150000):strip_icc()/Apr-apy-bank-hopes-cant-tell-difference_final-15cefe4dc77a4d81a02be1e2a26a4fac.png)