In the world of real estate financing, the "3/2/1 buy down" is a term that often piques the interest of both first-time homebuyers and seasoned investors. This mortgage option offers a unique opportunity to ease into the financial commitment of homeownership by temporarily reducing the interest rate. Understanding how a 3/2/1 buy down works can significantly impact your home-buying experience, making it more affordable and manageable. By diving into this topic, you can uncover strategies that might help you save money and reduce financial stress in the early years of your mortgage.

The 3/2/1 buy down plan is an appealing choice for those looking to lower their initial mortgage payments. It involves a structured reduction in the interest rate over the first three years of the loan, before reverting to the standard rate for the remainder of the term. This option is particularly popular among borrowers anticipating an increase in their income or those who wish to ease into their mortgage payments. By familiarizing yourself with the intricacies of the 3/2/1 buy down, you can better prepare for the financial responsibilities that come with owning a home.

In this comprehensive guide, we'll explore the mechanics of a 3/2/1 buy down, its benefits and drawbacks, and how it compares to other mortgage options. We'll delve into real-world scenarios to illustrate its potential advantages and provide insights into whether this option suits your financial situation. By the end of this article, you'll have a thorough understanding of the 3/2/1 buy down and how it might fit into your home-buying strategy.

Table of Contents

- Overview of the 3/2/1 Buy Down

- How the 3/2/1 Buy Down Works

- Benefits of a 3/2/1 Buy Down

- Potential Drawbacks

- Comparison with Other Mortgage Options

- Real-World Examples

- Eligibility Criteria

- Application Process

- Financial Planning with a 3/2/1 Buy Down

- Current Market Trends

- Expert Advice and Tips

- Case Studies

- Frequently Asked Questions

- External Resources

- Conclusion

Overview of the 3/2/1 Buy Down

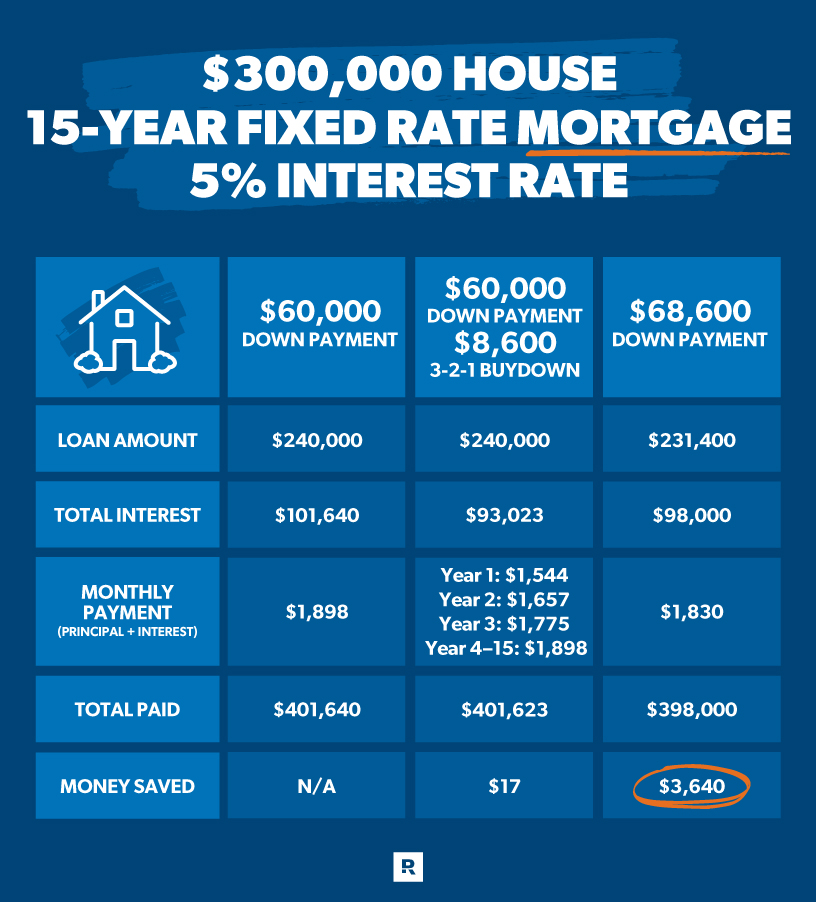

The 3/2/1 buy down is a type of mortgage arrangement designed to make homeownership more accessible in the initial years of a loan. It allows borrowers to benefit from a temporarily reduced interest rate, which decreases their monthly payments for the first three years. In the first year, the interest rate is reduced by 3%, by 2% in the second year, and by 1% in the third year. By the fourth year, the borrower begins paying the full interest rate agreed upon at the outset of the mortgage.

This structure is particularly advantageous for those who expect their income to grow, as it provides the flexibility to manage initial costs while planning for future financial stability. The 3/2/1 buy down is typically funded by the seller, lender, or a combination of both, who pay the difference in interest payments during the buy down period. It can be a strategic move in a buyer's market, where sellers are motivated to make their property more attractive by offering incentives like a buy down.

Understanding the 3/2/1 buy down requires familiarity with mortgage basics and the ability to assess its long-term implications. As with any financial decision, it's essential to weigh the pros and cons and consider personal financial goals. By doing so, borrowers can determine whether this mortgage option aligns with their circumstances and expectations for the future.

How the 3/2/1 Buy Down Works

The mechanics of a 3/2/1 buy down involve a tiered reduction in the interest rate, which results in lower monthly payments for the initial years of the loan. This reduction is not a permanent change to the interest rate but rather a temporary concession designed to ease the borrower's financial burden. To illustrate, consider a borrower who secures a 30-year fixed-rate mortgage at 5%. With a 3/2/1 buy down, their interest rate would be 2% in the first year, 3% in the second year, and 4% in the third year, before reverting to the standard 5% rate in the fourth year.

During these initial years, the lender or seller funds the difference between the reduced rate and the agreed-upon mortgage rate. This is typically accomplished through an escrow account set up at closing, where the necessary funds are deposited and used to subsidize the borrower's payments. The cost of a 3/2/1 buy down varies depending on the loan amount and the difference in interest rates, but it generally constitutes a percentage of the loan amount.

The appeal of a 3/2/1 buy down lies in its ability to offer substantial savings during the early years of homeownership. However, it's crucial for borrowers to understand that their payments will increase over time and plan accordingly. This means budgeting for higher payments and ensuring that future income aligns with these financial obligations. By doing so, borrowers can capitalize on the temporary relief provided by a 3/2/1 buy down while preparing for the long-term commitment of their mortgage.

Benefits of a 3/2/1 Buy Down

The primary benefit of a 3/2/1 buy down is the immediate reduction in monthly payments, which can significantly enhance a borrower's cash flow in the early years of a mortgage. This can be especially beneficial for first-time homebuyers or those with fluctuating incomes, as it provides the financial flexibility needed to adapt to new expenses associated with homeownership. By easing the financial burden upfront, borrowers can allocate funds to other priorities, such as furnishing their new home, making minor renovations, or building an emergency savings fund.

A 3/2/1 buy down can also serve as a strategic tool in competitive real estate markets. Sellers may offer a buy down to attract buyers, making their property stand out and increasing the likelihood of a sale. For buyers, this can mean obtaining a more favorable mortgage arrangement without additional cost. Additionally, lenders may use a buy down to entice borrowers, providing an added incentive to choose their loan products.

Beyond immediate financial relief, a 3/2/1 buy down can also align with long-term financial planning. Borrowers who anticipate salary increases or other income growth may find that the gradual increase in payments coincides with their evolving financial situation. This alignment can reduce the stress of adjusting to higher payments and contribute to a more sustainable approach to managing debt. Ultimately, the benefits of a 3/2/1 buy down extend beyond short-term savings, offering a flexible solution that can adapt to a borrower's changing financial landscape.

Potential Drawbacks

While a 3/2/1 buy down offers numerous advantages, it's not without potential drawbacks that borrowers should carefully consider. One of the primary concerns is the eventual increase in monthly payments once the buy down period concludes. Borrowers must be prepared for this adjustment and ensure that their financial situation can accommodate higher costs. Failure to do so could lead to financial strain and, in some cases, difficulty meeting mortgage obligations.

Another consideration is the cost associated with a 3/2/1 buy down. While sellers or lenders may cover the buy down expenses, this is not always the case. In some scenarios, borrowers might need to negotiate these terms or accept a higher purchase price to offset the seller's contribution. This can impact the overall cost of the home and should be factored into the decision-making process.

Moreover, borrowers should evaluate their long-term plans when considering a 3/2/1 buy down. If there's a possibility of refinancing or selling the home before the buy down period ends, the benefits may not outweigh the costs. Understanding the full scope of the financial commitment and how it aligns with future goals is crucial to making an informed decision. By weighing the potential drawbacks against the advantages, borrowers can determine whether a 3/2/1 buy down is the right fit for their circumstances.

Comparison with Other Mortgage Options

To fully appreciate the value of a 3/2/1 buy down, it's important to compare it with other mortgage options available to homebuyers. Fixed-rate and adjustable-rate mortgages (ARMs) are common alternatives, each with distinct characteristics that cater to different borrower needs. A fixed-rate mortgage offers predictability, with consistent monthly payments throughout the loan term. While this stability is appealing, it lacks the initial cost savings that a 3/2/1 buy down provides.

In contrast, an ARM features an interest rate that can fluctuate over time, based on market conditions. This can result in lower initial payments, similar to a buy down, but with the risk of future rate increases. While ARMs can be beneficial for short-term homeowners or those expecting interest rates to decrease, they require careful consideration of market trends and personal financial stability.

Another option to consider is an interest-only mortgage, where borrowers pay only the interest for a set period before transitioning to standard principal and interest payments. This can offer temporary relief but may lead to higher long-term costs. Ultimately, the best mortgage option depends on a borrower's financial goals, risk tolerance, and market conditions. By comparing these alternatives to a 3/2/1 buy down, borrowers can make an informed choice that aligns with their needs and expectations.

Real-World Examples

To provide a clearer picture of how a 3/2/1 buy down can benefit borrowers, let's explore some real-world examples. Consider a young couple purchasing their first home. They secure a 30-year fixed-rate mortgage at 6%, but with a 3/2/1 buy down, their interest rate is reduced to 3% in the first year. This significantly lowers their monthly payments, allowing them to allocate funds toward home improvements and savings.

As their careers advance, they anticipate salary increases that will coincide with the gradual rise in their mortgage payments. By the fourth year, they're financially prepared to handle the full payment, thanks to careful budgeting and planning during the buy down period. This strategic approach enables them to enjoy the benefits of homeownership without compromising their financial security.

In another scenario, a seasoned investor uses a 3/2/1 buy down to acquire a rental property. The reduced payments in the initial years allow for greater cash flow, which is reinvested into property enhancements and marketing efforts. This strategy increases the property's value and appeal, ultimately leading to higher rental income. By the time the buy down period ends, the investor has established a strong revenue stream that comfortably covers the full mortgage payments.

These examples illustrate the potential advantages of a 3/2/1 buy down, demonstrating its versatility and applicability across different financial situations. By understanding these scenarios, borrowers can better assess how this mortgage option might fit into their home-buying strategy and financial goals.

Eligibility Criteria

Eligibility for a 3/2/1 buy down depends on several factors, including the lender's policies and the borrower's financial profile. Lenders typically require a stable income, a good credit score, and a reasonable debt-to-income ratio to qualify for this mortgage option. Additionally, the property must meet certain criteria, such as being a primary residence or an investment property, to be eligible for a buy down.

Borrowers should also consider the seller's willingness to participate in a buy down, as this can influence the overall cost and feasibility of the arrangement. In some cases, sellers may be more inclined to offer a buy down in a buyer's market, where competition is high, and incentives are necessary to attract potential buyers.

Understanding the eligibility criteria is crucial for borrowers considering a 3/2/1 buy down. By reviewing their financial situation and discussing options with a lender, they can determine whether this mortgage arrangement aligns with their needs and qualifications. This proactive approach ensures a smooth application process and increases the likelihood of securing favorable terms.

Application Process

The application process for a 3/2/1 buy down is similar to that of a standard mortgage but includes additional considerations related to the buy down arrangement. Borrowers must first gather necessary financial documentation, such as proof of income, credit reports, and bank statements, to demonstrate their ability to meet mortgage obligations.

Next, borrowers should consult with their lender to discuss the specifics of the 3/2/1 buy down, including the interest rate reductions and any associated costs. This conversation will clarify the terms and conditions and help borrowers understand their financial responsibilities during and after the buy down period.

Once the details are finalized, borrowers should prepare for the closing process, where the buy down funds are typically deposited into an escrow account. This ensures that the necessary payments are made to subsidize the borrower's mortgage payments during the buy down period. By understanding the application process, borrowers can navigate the complexities of securing a 3/2/1 buy down with confidence and ease.

Financial Planning with a 3/2/1 Buy Down

Effective financial planning is essential for maximizing the benefits of a 3/2/1 buy down. Borrowers should begin by evaluating their current financial situation and projecting future income growth to ensure they can comfortably transition to higher mortgage payments after the buy down period. This involves creating a budget that accounts for anticipated expenses and savings goals, allowing for a seamless adjustment to changing financial obligations.

Additionally, borrowers should consider the impact of potential interest rate changes on their mortgage and explore refinancing options if rates become more favorable. By staying informed about market trends and maintaining a flexible financial strategy, borrowers can optimize their mortgage arrangement and achieve their long-term homeownership goals.

Regularly reviewing and adjusting financial plans is crucial for maintaining stability and achieving success with a 3/2/1 buy down. By proactively managing their finances, borrowers can enjoy the benefits of this mortgage option while preparing for future challenges and opportunities.

Current Market Trends

Market trends play a significant role in the popularity and feasibility of a 3/2/1 buy down. During periods of low interest rates, borrowers may find less need for buy downs, as standard mortgage rates are already affordable. However, in rising rate environments, a 3/2/1 buy down can offer a valuable solution for managing costs in the initial years of a mortgage.

Economic factors, such as inflation and employment rates, also influence the housing market and the availability of buy down options. In competitive markets, sellers may be more inclined to offer buy downs as incentives to attract buyers, while lenders may adjust their policies to align with market demands.

Staying informed about current market trends is essential for borrowers considering a 3/2/1 buy down. By understanding the broader economic landscape and its impact on mortgage rates and availability, borrowers can make informed decisions that align with their financial goals and market conditions.

Expert Advice and Tips

Expert advice can be invaluable for borrowers navigating the complexities of a 3/2/1 buy down. Financial advisors and mortgage professionals can provide insights into the advantages and drawbacks of this mortgage option, helping borrowers make informed decisions that align with their financial goals.

One key piece of advice is to thoroughly understand the terms and conditions of the 3/2/1 buy down arrangement, including the impact on monthly payments and the overall cost of the mortgage. Borrowers should also consider their long-term plans and how a buy down fits into their financial strategy, including potential refinancing options and future income growth.

By seeking expert guidance and conducting thorough research, borrowers can confidently navigate the mortgage process and secure a 3/2/1 buy down that meets their needs and expectations.

Case Studies

Case studies offer valuable insights into the real-world application of a 3/2/1 buy down. By examining the experiences of borrowers who have utilized this mortgage option, readers can gain a deeper understanding of its benefits and challenges.

In one case study, a young family used a 3/2/1 buy down to purchase their first home. The reduced payments in the initial years allowed them to build a solid financial foundation, while the gradual increase in payments aligned with their growing income. This strategic approach enabled them to enjoy the benefits of homeownership without compromising their financial stability.

Another case study highlights an investor who leveraged a 3/2/1 buy down to acquire a rental property. The reduced payments provided greater cash flow, which was reinvested into property improvements and marketing efforts. This strategy increased the property's value and appeal, ultimately leading to higher rental income and a successful investment.

These case studies demonstrate the versatility and potential advantages of a 3/2/1 buy down, providing valuable insights for borrowers considering this mortgage option.

Frequently Asked Questions

What is a 3/2/1 buy down?

A 3/2/1 buy down is a mortgage arrangement where the interest rate is temporarily reduced for the first three years of the loan, resulting in lower monthly payments. In the first year, the rate is reduced by 3%, by 2% in the second year, and by 1% in the third year, before reverting to the standard rate in the fourth year.

Who pays for the buy down?

The buy down is typically funded by the seller, lender, or a combination of both. In some cases, the borrower may negotiate these terms as part of the home purchase agreement.

Are there any drawbacks to a 3/2/1 buy down?

The main drawback is the eventual increase in monthly payments after the buy down period. Borrowers must be prepared for this adjustment and ensure their financial situation can accommodate higher costs.

How does a 3/2/1 buy down compare to other mortgage options?

A 3/2/1 buy down offers temporary cost savings, unlike fixed-rate mortgages, which provide consistent payments. It differs from adjustable-rate mortgages (ARMs), which have fluctuating rates based on market conditions.

What should I consider before choosing a 3/2/1 buy down?

Consider your financial goals, income growth projections, and long-term plans. Evaluate whether the temporary cost savings align with your needs and whether you're prepared for higher payments after the buy down period.

Can I refinance after a 3/2/1 buy down?

Yes, refinancing is possible after a 3/2/1 buy down, but consider market conditions and potential costs before making this decision. Refinancing may offer more favorable terms if interest rates decrease.

External Resources

For further information on 3/2/1 buy down mortgages and other financial topics, consider exploring these external resources:

- Consumer Financial Protection Bureau - Offers guidance on mortgage options and financial planning.

- Investopedia - Provides comprehensive articles on a wide range of financial topics, including mortgages.

Conclusion

The 3/2/1 buy down is a versatile mortgage option that offers temporary financial relief by reducing interest rates in the early years of a loan. It can be an attractive choice for first-time homebuyers, investors, and those anticipating income growth. By understanding its mechanics, benefits, and potential drawbacks, borrowers can determine if a 3/2/1 buy down aligns with their financial goals and market conditions. With careful planning and expert guidance, this mortgage option can provide a strategic path to successful homeownership.

You Might Also Like

Predicting The Next Meme Coin To Explode: A Complete GuideEvaluating FFIE: Is It A Smart Investment Choice?

Aaron Erter: A Visionary Leader Shaping The Future

Does Vaporizing Weed Smell: Myths And Facts Uncovered

Starbucks Stock Dynamics: Investment Analysis And Insights

Article Recommendations

- Stephanie Ike Net Worth An Insightful Analysis

- Senate Leader Mitch Mcconnell Resigns Impact Next Steps

- Emiru Sick Latest Updates Amp News