A HELOC, essentially, is a line of credit secured by the equity in your home. Unlike traditional loans, it allows for withdrawal of funds as needed, similar to using a credit card. The structure of HELOCs typically consists of a draw period, during which funds can be accessed and interest-only payments are made, followed by a repayment period where principal payments are required. This setup offers flexibility, but it also demands a thorough understanding of the responsibilities and potential risks involved. When opting for HELOC interest-only payments, homeowners can experience significant short-term savings. By only paying the interest, monthly payments remain low during the draw period. This can be particularly beneficial for those facing temporary financial constraints, or those looking to allocate capital elsewhere. However, it is essential to maintain a comprehensive financial plan to ensure that the eventual principal repayment does not become burdensome. As with any financial decision, understanding the terms and planning ahead are key to leveraging the benefits of HELOC interest-only payments.

Table of Contents

- Understanding HELOCs

- The Structure of a HELOC

- What Are Interest-Only Payments?

- Benefits of Interest-Only Payments

- Potential Risks of Interest-Only Payments

- Eligibility Requirements for a HELOC

- Comparison with Other Loans

- Importance of Financial Planning

- Tax Implications

- Managing Your HELOC Effectively

- Common Misconceptions

- Real-Life Scenarios

- Frequently Asked Questions

- Conclusion

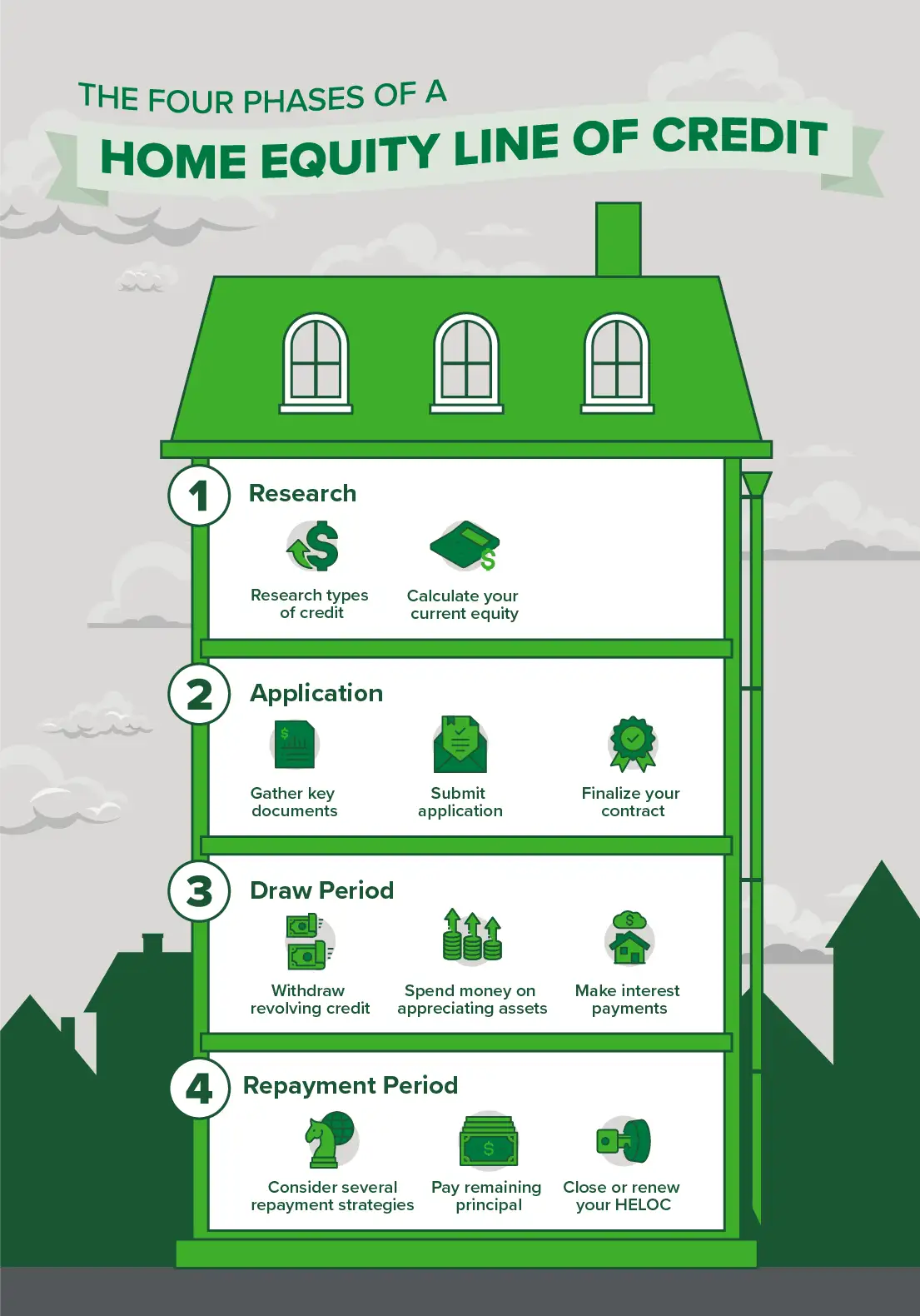

Understanding HELOCs

A Home Equity Line of Credit (HELOC) is a revolving credit line that allows homeowners to borrow against the equity of their home. Unlike a traditional loan that provides a lump sum, a HELOC offers flexibility by allowing borrowers to withdraw funds as needed, up to a certain limit. This makes HELOCs a popular choice for those looking to finance ongoing projects or manage unforeseen expenses.

HELOCs are structured similarly to credit cards in that they have a credit limit and require payments only on the amount borrowed. However, because they are secured by the home, they typically offer lower interest rates than unsecured lines of credit. The amount you can borrow is determined by the equity you have in your home, which is the difference between your home’s appraised value and the balance of your mortgage.

The interest rates on HELOCs are usually variable, meaning they can fluctuate with changes in the market index. This variability can affect the monthly payment amount, making it crucial for homeowners to stay informed about market trends. Despite this, HELOCs remain an attractive option for many due to their flexibility and potential tax benefits.

The Structure of a HELOC

The structure of a HELOC consists of two main periods: the draw period and the repayment period. Understanding these phases is essential for effectively managing the line of credit.

Draw Period: During this time, homeowners can borrow from the credit line up to the approved limit. This period usually lasts between 5 to 10 years. Interest-only payments are typically required during this time, allowing for lower monthly payments. This flexibility can be advantageous for those needing temporary financial relief or those managing other investments.

Repayment Period: Once the draw period ends, the HELOC enters the repayment phase. This period typically spans 10 to 20 years, during which homeowners must repay both the principal and interest. Monthly payments increase during this phase, as they now include principal repayment. It’s crucial to plan for this transition to avoid financial strain.

Additionally, some lenders offer the option to renew or extend the draw period, but this often involves a credit re-evaluation and may not be guaranteed. Understanding these structural components helps homeowners prepare financially and make informed decisions about their HELOC usage.

What Are Interest-Only Payments?

Interest-only payments are a unique feature of HELOCs that allow borrowers to pay only the interest on the principal balance during the draw period. This payment structure can significantly reduce monthly payments, offering financial flexibility and freeing up cash flow for other uses.

For example, if a homeowner has a HELOC with a principal balance of $50,000 and an interest rate of 5%, their monthly interest-only payment would be approximately $208.33. This method allows homeowners to reduce their monthly financial obligations, making it easier to manage other expenses or investments.

However, it’s important to note that interest-only payments do not reduce the principal balance. This means that once the draw period ends, the principal amount will still need to be repaid, often resulting in higher monthly payments during the repayment phase. Understanding this dynamic is crucial for effective financial planning.

Benefits of Interest-Only Payments

Opting for interest-only payments on a HELOC offers several advantages, particularly for those seeking flexibility in their financial planning.

- Lower Monthly Payments: During the draw period, making only interest payments can significantly reduce monthly obligations, providing more disposable income for other financial needs.

- Cash Flow Management: Interest-only payments free up cash flow, allowing homeowners to allocate funds to other investments or pay down higher-interest debt.

- Financial Flexibility: This payment structure offers flexibility, enabling homeowners to adjust their financial strategies as needed and manage unexpected expenses more effectively.

- Short-Term Relief: For those facing temporary financial challenges, interest-only payments provide short-term relief without the burden of high monthly payments.

These benefits make interest-only payments an attractive option for many homeowners. However, it’s important to approach this strategy with caution and ensure that a plan is in place for the eventual repayment of the principal balance.

Potential Risks of Interest-Only Payments

While interest-only payments offer several advantages, they also come with potential risks that should not be overlooked.

- Increased Long-Term Costs: By delaying principal repayment, the overall cost of the loan can increase over time, especially if interest rates rise during the draw period.

- Higher Future Payments: Once the draw period ends, monthly payments can increase significantly due to the need to repay the principal, which may strain finances if not adequately planned for.

- Market Fluctuations: As HELOCs often have variable interest rates, fluctuations in the market index can lead to unpredictable changes in monthly payments.

- Equity Depletion: Relying heavily on interest-only payments can deplete home equity over time, potentially reducing the value of the property as a financial asset.

Understanding these risks is vital for homeowners considering interest-only payments. A well-thought-out financial plan can help mitigate these risks and ensure that the benefits of interest-only payments are maximized.

Eligibility Requirements for a HELOC

To qualify for a HELOC, homeowners must meet certain eligibility criteria set by lenders. These requirements typically include:

- Equity in the Home: Lenders usually require a minimum level of equity in the property, often around 15-20% of the home's appraised value.

- Credit Score: A good credit score is essential, with most lenders requiring a score of 620 or higher to qualify for a HELOC.

- Debt-to-Income Ratio: Lenders typically look for a debt-to-income ratio below 43%, ensuring that homeowners can manage additional debt obligations.

- Proof of Income: Homeowners must provide evidence of a stable income to demonstrate their ability to repay the line of credit.

Meeting these requirements is crucial for securing a HELOC. Homeowners should assess their financial situation and consult with lenders to determine their eligibility and explore the best options available.

Comparison with Other Loans

HELOCs offer a distinct set of features compared to other types of loans, making them a unique financial tool for homeowners. Understanding how they compare with other options is essential for making informed decisions.

- HELOC vs. Home Equity Loan: While both are secured by home equity, a home equity loan provides a lump sum with fixed payments, whereas a HELOC offers a revolving line of credit with variable payments. HELOCs provide more flexibility, but home equity loans offer more predictable payments.

- HELOC vs. Personal Loan: Personal loans are unsecured and typically have higher interest rates. HELOCs, being secured by the home, usually offer lower rates and higher borrowing limits, making them a more cost-effective option for larger expenses.

- HELOC vs. Credit Card: Credit cards are unsecured and come with higher interest rates and lower limits. HELOCs provide more favorable terms and are better suited for financing significant expenses or projects.

Considering these comparisons helps homeowners determine the most suitable financial tool for their needs, taking into account factors such as interest rates, payment structures, and borrowing limits.

Importance of Financial Planning

Financial planning is crucial when utilizing a HELOC, particularly when opting for interest-only payments. A comprehensive plan can help mitigate risks and ensure that homeowners are prepared for future financial obligations.

Effective financial planning involves:

- Budgeting: Creating a detailed budget that includes projected expenses and income, allowing homeowners to manage their cash flow effectively.

- Setting Goals: Establishing short-term and long-term financial goals to guide spending and saving decisions.

- Contingency Planning: Preparing for unforeseen circumstances, such as market fluctuations or changes in income, to avoid financial strain.

- Monitoring Interest Rates: Staying informed about market trends and potential changes in interest rates to adjust financial strategies accordingly.

By prioritizing financial planning, homeowners can make the most of their HELOC and interest-only payment structure while safeguarding their long-term financial health.

Tax Implications

HELOCs may offer certain tax benefits, but it’s essential to understand the specific implications and eligibility criteria.

The Tax Cuts and Jobs Act of 2017 limited the deductibility of interest on home equity loans and lines of credit. However, interest on a HELOC may still be deductible if the funds are used for significant home improvements. Homeowners should consult with a tax professional to determine their eligibility for any deductions and ensure compliance with tax regulations.

Understanding these tax implications can help homeowners maximize the financial advantages of a HELOC and make informed decisions about their use.

Managing Your HELOC Effectively

Effective management of a HELOC is crucial for maximizing its benefits and minimizing potential risks. Here are some strategies for managing a HELOC effectively:

- Regular Monitoring: Keep track of the outstanding balance and interest rates to ensure that payments remain manageable and within budget.

- Timely Payments: Make timely payments to avoid late fees and negative impacts on credit scores.

- Avoid Overborrowing: Borrow only what is necessary to prevent excessive debt and ensure that repayment remains feasible.

- Plan for Repayment: Develop a strategy for repaying the principal balance once the draw period ends to avoid financial strain.

By implementing these strategies, homeowners can effectively manage their HELOC and enjoy its benefits while safeguarding their financial future.

Common Misconceptions

There are several misconceptions surrounding HELOCs and interest-only payments that can lead to confusion and misinformed decisions.

- Misconception 1: Interest-only payments reduce the principal balance – In reality, these payments only cover the interest, leaving the principal untouched.

- Misconception 2: HELOCs are only for emergencies – While they can be used for emergencies, HELOCs are also valuable for planned expenses, such as home improvements or education costs.

- Misconception 3: HELOCs are risk-free – Like any financial tool, HELOCs come with risks, particularly if interest rates rise or if the homeowner’s financial situation changes.

Understanding these misconceptions can help homeowners make informed decisions and leverage HELOCs effectively as part of their financial strategy.

Real-Life Scenarios

Real-life scenarios can provide valuable insights into how homeowners utilize HELOCs and interest-only payments to meet their financial goals.

Scenario 1: A homeowner uses a HELOC to fund a major home renovation project. By opting for interest-only payments during the draw period, they maintain low monthly payments while investing in their property’s value.

Scenario 2: Another homeowner uses a HELOC to consolidate high-interest credit card debt. The lower interest rate of the HELOC allows them to reduce their overall interest expenses while managing their cash flow more effectively.

These scenarios demonstrate the diverse applications of HELOCs and interest-only payments, highlighting their flexibility and potential benefits for homeowners.

Frequently Asked Questions

- What is the primary advantage of HELOC interest-only payments? The primary advantage is lower monthly payments during the draw period, providing financial flexibility and freeing up cash flow for other expenses.

- Can interest rates on a HELOC change? Yes, most HELOCs have variable interest rates that can fluctuate with market conditions, affecting monthly payments.

- Are there any tax benefits to using a HELOC? Interest on a HELOC may be tax-deductible if the funds are used for significant home improvements, but homeowners should consult a tax professional to confirm eligibility.

- How can I ensure I’m eligible for a HELOC? To qualify, ensure you have sufficient home equity, a good credit score, a low debt-to-income ratio, and proof of stable income.

- What happens when the draw period of a HELOC ends? The HELOC enters the repayment period, requiring repayment of both the principal and interest, often resulting in higher monthly payments.

- Can a HELOC be used for purposes other than home improvements? Yes, a HELOC can be used for various purposes, such as debt consolidation, education expenses, or emergency funds.

Conclusion

HELOC interest-only payments offer homeowners a flexible financial tool for managing cash flow and meeting various financial needs. By understanding the structure, benefits, and potential risks, homeowners can make informed decisions about using this option to their advantage. Effective financial planning and management are essential for maximizing the benefits of a HELOC while minimizing potential drawbacks. As with any financial decision, consulting with professionals and staying informed about market trends can help homeowners leverage HELOCs effectively and achieve their financial goals.

You Might Also Like

Significance And Value Of The Spirit Of 76 CoinJim Reinhart: A Visionary Leader In The Business World

Paul T Cappuccio: A Visionary Corporate Leader

Neal Sample's Role At Walgreens: Insights And Impact

Trxade Stock: Latest Developments And Market Insights

Article Recommendations

- Don Jr Kimberly Guilfoyle Photos Informational Details Insights

- Jim Jackson Mavericks Dallas Legend Remembers The Glory Days

- Is Megan Fox Bisexual Exploring Her Sexuality