Investing in mutual funds has gained immense popularity among individuals seeking to grow their wealth over time. Among the myriad of options available, two primary categories stand out: direct and regular mutual funds. Understanding the differences between the two can significantly impact your investment strategy and returns. This comprehensive guide will delve into the intricacies of direct vs regular mutual funds, providing insights to help you make informed decisions.

Direct and regular mutual funds cater to different types of investors, each offering unique benefits and drawbacks. While both are essentially the same in terms of the underlying investment, the way they are purchased and managed can lead to variations in cost and performance. In this article, we'll explore these differences, alongside the advantages and disadvantages of each, helping you decide which option aligns best with your financial goals.

Whether you're a novice investor or have years of experience, understanding the distinction between direct and regular mutual funds is crucial. By the end of this guide, you'll have a clearer picture of which path suits your investment needs, ensuring that your money works harder for you. Let's dive into the world of mutual funds and uncover the best approach for your portfolio.

Table of Contents

- Understanding Mutual Funds

- What are Direct Mutual Funds?

- What are Regular Mutual Funds?

- Key Differences Between Direct and Regular Mutual Funds

- Cost Comparison: Direct vs Regular

- Performance Impact on Investments

- Advantages of Direct Mutual Funds

- Advantages of Regular Mutual Funds

- Disadvantages of Direct Mutual Funds

- Disadvantages of Regular Mutual Funds

- How to Choose Between Direct and Regular Mutual Funds

- Role of Financial Advisors in Mutual Fund Investment

- Tax Implications of Mutual Fund Investments

- Frequently Asked Questions

- Conclusion

Understanding Mutual Funds

Mutual funds are investment vehicles that pool money from multiple investors to purchase a diversified portfolio of stocks, bonds, or other securities. Managed by professional fund managers, mutual funds aim to provide investors with diversified exposure to various asset classes, thereby reducing risk and potentially enhancing returns. They offer a convenient option for individuals who may not have the time or expertise to manage their own investments.

Investors can choose from various types of mutual funds, including equity, debt, hybrid, and money market funds, each designed to meet specific investment objectives. These funds are regulated by financial authorities, ensuring transparency and protection for investors.

What are Direct Mutual Funds?

Direct mutual funds are purchased directly from the fund house, without the involvement of intermediaries such as brokers or distributors. As a result, investors do not incur any commission expenses, leading to lower expense ratios compared to regular funds. This cost-saving advantage can significantly enhance the overall returns on investments over the long term.

With direct mutual funds, investors take on the responsibility of conducting their research and making informed decisions about their investments. This option is ideal for individuals who are knowledgeable about the market and prefer to have greater control over their investment choices.

What are Regular Mutual Funds?

Regular mutual funds are purchased through intermediaries, such as brokers or financial advisors, who receive a commission for their services. This commission is factored into the fund's expense ratio, making regular funds slightly more expensive than their direct counterparts. However, the expertise and guidance provided by intermediaries can be invaluable for investors seeking personalized advice and support.

Regular mutual funds are suitable for individuals who may not have the time or expertise to manage their investments independently. By leveraging the knowledge of financial advisors, investors can benefit from tailored investment strategies and ongoing support.

Key Differences Between Direct and Regular Mutual Funds

While both direct and regular mutual funds share the same underlying investments, there are key differences that set them apart. One of the most notable distinctions is the cost structure, with direct funds typically having lower expense ratios due to the absence of intermediary commissions. This cost advantage can lead to higher net returns for investors over time.

Another significant difference lies in the level of investor involvement. Direct fund investors are responsible for conducting their research and making investment decisions, while regular fund investors receive guidance and support from financial advisors. This distinction can influence the level of control and autonomy investors have over their portfolios.

Additionally, the process of purchasing and managing investments varies between the two options. Direct fund investors interact directly with the fund house, while regular fund investors work with intermediaries to execute transactions and manage their accounts.

Cost Comparison: Direct vs Regular

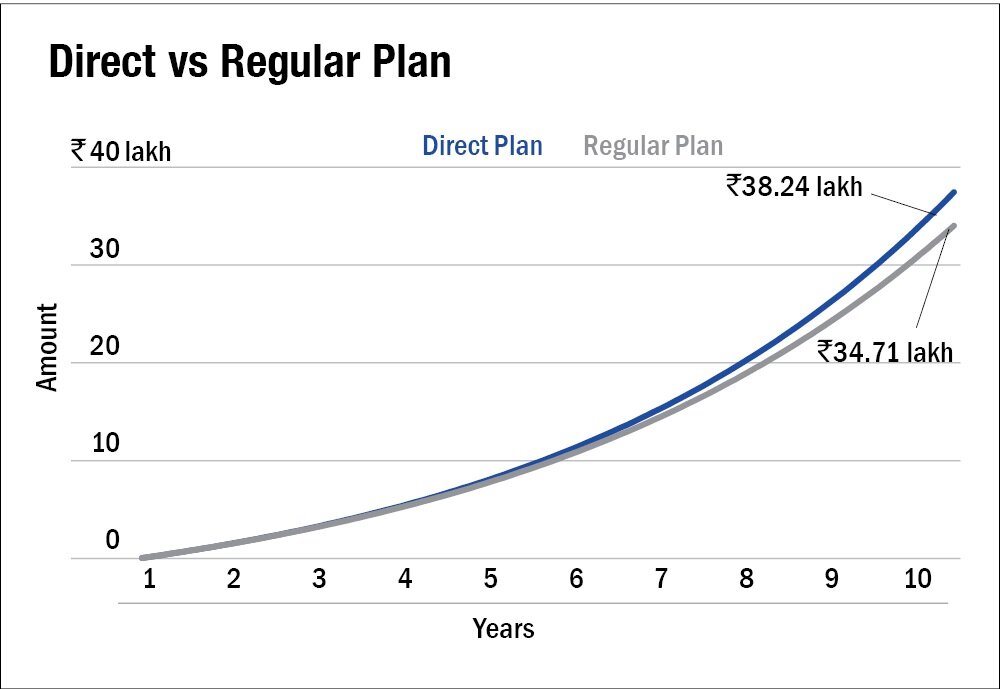

Cost is a crucial factor in determining the long-term returns of mutual fund investments. Direct mutual funds generally have lower expense ratios compared to regular funds, as they eliminate the need for intermediary commissions. This cost-saving advantage can translate into higher returns for investors over time.

For example, if a direct fund has an expense ratio of 1% and a regular fund has an expense ratio of 1.5%, the difference may seem negligible initially. However, over the course of several years, this 0.5% difference can compound, resulting in a significant impact on the overall returns.

Investors should carefully consider the cost implications of their investment choices, as even small differences in expense ratios can have a substantial effect on long-term wealth accumulation.

Performance Impact on Investments

The performance of mutual funds can be influenced by various factors, including market conditions, fund management strategies, and expense ratios. While direct and regular funds share the same underlying investments, the lower expense ratios of direct funds can lead to slightly higher net returns over time.

However, it's important to note that the expertise and guidance provided by financial advisors in regular funds can also contribute to performance. Advisors may offer valuable insights and recommendations that align with an investor's financial goals and risk tolerance.

Ultimately, the choice between direct and regular funds should be based on an investor's preference for cost savings versus professional guidance, as well as their level of involvement in managing their investments.

Advantages of Direct Mutual Funds

Direct mutual funds offer several advantages to investors, primarily centered around cost savings and control over investment decisions. By eliminating intermediary commissions, direct funds have lower expense ratios, which can enhance net returns over time. This cost advantage is particularly beneficial for long-term investors seeking to maximize their wealth accumulation.

In addition to cost savings, direct fund investors have greater autonomy and control over their investment choices. They can conduct their research, select funds that align with their financial goals, and make informed decisions about their portfolios.

Moreover, direct funds offer transparency, allowing investors to have a clear understanding of the investments they hold and the associated costs. This transparency can lead to more informed decision-making and greater confidence in their investment strategies.

Advantages of Regular Mutual Funds

Regular mutual funds provide investors with access to professional guidance and support, which can be invaluable for individuals who may not have the time or expertise to manage their investments independently. Financial advisors offer personalized advice and recommendations, helping investors develop tailored investment strategies that align with their financial goals and risk tolerance.

Additionally, the expertise of financial advisors can enhance investment performance by providing insights into market trends and opportunities. Advisors can also assist with rebalancing portfolios, managing risk, and optimizing returns.

For investors seeking ongoing support and personalized advice, regular mutual funds offer a valuable solution that can simplify the investment process and provide peace of mind.

Disadvantages of Direct Mutual Funds

While direct mutual funds offer cost savings and greater control, they also come with certain disadvantages. One of the primary challenges is the need for investors to conduct their research and make informed decisions independently. This level of involvement may not be suitable for individuals who lack the time or expertise to manage their investments effectively.

Additionally, direct fund investors may miss out on the personalized advice and guidance provided by financial advisors, which can be particularly valuable in navigating complex market conditions and developing tailored investment strategies.

Investors considering direct funds should carefully evaluate their ability to manage their investments independently and consider the potential trade-offs in terms of professional support and guidance.

Disadvantages of Regular Mutual Funds

Regular mutual funds, while offering professional guidance, come with higher expense ratios due to the inclusion of intermediary commissions. These additional costs can erode net returns over time, particularly for long-term investors seeking to maximize their wealth accumulation.

Furthermore, the reliance on financial advisors may limit an investor's control and autonomy over their investment choices. Investors may need to balance the benefits of professional support with the desire for greater involvement in managing their portfolios.

It's essential for investors to weigh the cost implications and potential limitations of regular funds against the benefits of personalized advice and guidance, ensuring that their investment decisions align with their financial goals.

How to Choose Between Direct and Regular Mutual Funds

Choosing between direct and regular mutual funds requires careful consideration of an investor's financial goals, risk tolerance, and level of involvement in managing investments. While direct funds offer cost savings and greater control, regular funds provide access to professional guidance and support.

Investors should assess their ability to conduct research and make informed decisions independently, as well as their preference for personalized advice and support. Additionally, evaluating the cost implications and potential impact on long-term returns is crucial in making an informed choice.

By carefully weighing the advantages and disadvantages of each option, investors can select the mutual fund type that aligns with their investment strategy and financial objectives.

Role of Financial Advisors in Mutual Fund Investment

Financial advisors play a pivotal role in mutual fund investment, offering personalized advice and guidance to help investors achieve their financial goals. Advisors provide insights into market trends, investment opportunities, and risk management strategies, ensuring that investors make informed decisions.

Additionally, financial advisors assist with portfolio rebalancing, optimizing returns, and managing risk. They serve as valuable resources for investors seeking to navigate complex market conditions and develop tailored investment strategies.

By leveraging the expertise of financial advisors, investors can benefit from professional support and guidance, simplifying the investment process and enhancing overall performance.

Tax Implications of Mutual Fund Investments

Understanding the tax implications of mutual fund investments is crucial for investors seeking to maximize their returns and minimize tax liabilities. Depending on the type of mutual fund and the holding period, investors may be subject to capital gains tax, dividend distribution tax, or other tax obligations.

Equity funds held for more than one year typically qualify for long-term capital gains tax, while those held for less than one year are subject to short-term capital gains tax. Debt funds, on the other hand, have different tax treatment, with long-term gains taxed at a lower rate and short-term gains taxed as regular income.

Investors should consider the tax implications of their investment choices and consult with financial advisors or tax professionals to develop strategies that optimize their tax efficiency and overall returns.

Frequently Asked Questions

- What is the main difference between direct and regular mutual funds?

The main difference lies in the cost structure. Direct funds have lower expense ratios as they are purchased directly from the fund house, eliminating intermediary commissions. Regular funds involve intermediaries, leading to slightly higher costs.

- Are direct mutual funds better than regular mutual funds?

It depends on the investor's preference for cost savings versus professional guidance. Direct funds offer cost advantages, while regular funds provide personalized advice and support.

- Can I switch from a regular mutual fund to a direct mutual fund?

Yes, investors can switch from regular to direct funds, but it's essential to consider any exit loads or tax implications before making the transition.

- How do I purchase direct mutual funds?

Direct mutual funds can be purchased directly from the fund house's website or through online investment platforms. Investors need to conduct their research and make informed decisions independently.

- Do direct mutual funds have any hidden charges?

No, direct mutual funds are transparent in terms of charges, with no hidden fees. The expense ratio is lower as there are no intermediary commissions.

- Is professional guidance necessary for mutual fund investments?

While professional guidance can be beneficial, it's not mandatory. Investors with sufficient knowledge and expertise can manage their investments independently, while others may prefer the support of financial advisors.

Conclusion

In the debate between direct vs regular mutual funds, the choice ultimately depends on an investor's individual preferences and financial objectives. Direct mutual funds offer cost savings and greater control, making them ideal for knowledgeable investors who prefer to manage their own portfolios. On the other hand, regular mutual funds provide access to professional guidance and personalized advice, catering to individuals seeking support and tailored investment strategies.

By carefully considering the advantages and disadvantages of each option, investors can make informed decisions that align with their goals and risk tolerance. Whether opting for direct or regular mutual funds, the key is to develop a well-thought-out investment strategy that maximizes returns and supports long-term wealth accumulation.

For further insights and guidance on mutual fund investments, consider consulting with a financial advisor or exploring reputable resources such as Investopedia.

You Might Also Like

Steve Stagner: Business Leadership And InsightsNXP Layoffs 2024: Ensuring Future Growth Amidst Challenges

Inside The Life And Career Of Steven J Moskowitz: A Legal Luminary

Future Prospects: Cowi Stock Price Prediction Analysis

Douglas L. Becker: A Visionary Leader In Education And Business

Article Recommendations

- Malibu Fire Kristys House Update Aftermath

- Meet Kokinnakis The Tennis Player

- Real Madrid Vs Atalanta Live Stats And Indepth Analysis